We believe these challenges may best be answered through the effective use of an evolved ‘full-service’ managed service provider (MSP). To test this hypothesis, GFT and Broadridge have formed an industry working group to define a future state model, and this paper explores the existing market challenges and our blueprint for this new efficient model.

Introduction

Operational areas of banks and corporate institutions have adopted multiple strategies to lower FX operational costs, including moving operational processing to lower cost nearshore and offshore locations. However, the pressure for institutions to reduce cost further and improve their cost/income ratios is not abating. Return on Equity (ROE) is decreasing and many firms have already leveraged the efficiency of traditional variable cost models. A recent report by Analyst firm Coalition suggests that banks saw an ROE of just 6.7 per cent in 2015, down from 9.2 per cent the year before. This was below the businesses’ cost of capital of at least 10 per cent, and the mid-teen percentage returns to which their investors aspire. Unlike other markets – witness the number of banks exiting commodities units due to increased costs of doing business – banks cannot simply close down FX units or fully outsource the function. The challenge is clear – how do you operate in a business that remains ‘mandatory’ for a bank whilst securing an acceptable cost base?

This dilemma is forcing a fundamental shift in the search for business solutions that can build on the industry trend for the mutualisation of cost models, where a common facility is shared or operated by many market participants.

Whilst most firms have invested in front office platforms to deliver higher volumes of trades, there has been a general lack of investment in middle and back office technology and operational processing. The result has been a reliance on legacy systems that are not scalable, prone to manual intervention and increased trade failures. Capital investments required to remedy this can be partly mitigated by outsourcing.

FX operations took a leap forward in 2002 with the launch of CLS (for multi-currency cash settlements) covering spot, forwards and vanilla swaps to mitigate so-called ‘Herstatt Risk’. This covers the majority of the STP market which is a high volume but low margin business. However, the ‘80:20’ rule is applicable here – broadly speaking the non-CLS FX and OTC transactions cover 20% of total transactions but create 80% of the processing touch points for operational units.

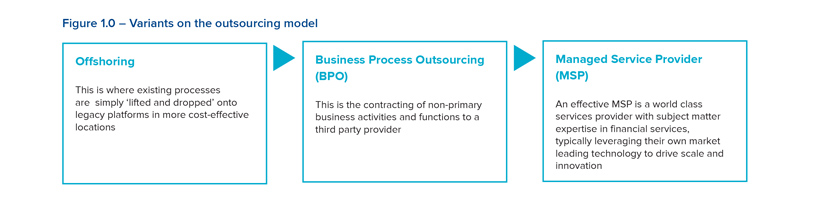

A precedent in the market to achieve the mutualisation of cost models has been set by the rise of these models in other non-financial industries e.g. telecommunications, where broadband infrastructure is shared across multiple networks. Organisations seeking to transform ROE should consider the pooling of resources and technology into managed services that can achieve the economies of scale and the mutualisation of standards, data and process, as well as their readiness for the new distributed ledger and other fintech technologies as they emerge. There is a wave of ‘open standards’ that is emerging e.g. Open Banking Standards (UK Treasury) and the European PSD2 (crossborder faster payments). If market participants are processing in the same way, then the argument for consolidation/ mutualisation gets stronger. This unified means of processing transactions allows for the Managed Service Provider (MSP) – see Figure 1.0 on page 3 – to be front and centre in driving and shaping how this new technology is used and integrated into the financial ecosystem, as well as enabling its accessibility.

The FX Volume Versus Margin Spectrum

The illustration on the next page (Figure 3.0) shows segmentation in the FX market, namely between the interbank and the non-interbank market. The market ranges from highly automated interbank CLS activity to corporate/nonfinancial customers often requiring high cost, operationally risky and manual intervention. Breaking this down further, interbank dealers represent (31%) of volume, banks (19%), other financial customers (40%) and non-financial customers (9%). The opportunity is to develop economies of scale by reducing the manual intervention in trade support and pooling together volume to enable a scalable single platform processing model, covering operations for both CLS and non-CLS transactions.

Current FX Operational Cost

Change budgets are increasingly focused on meeting waves of new regulatory requirements; however, this is mainly being achieved through the addition of processes, controls and reporting on top of already offshored inefficient processes that sit on legacy infrastructure. No one has the mandate to fundamentally implement a Six Sigma agile business process reengineering project to the current business: instead change effort is limited to small-scale efficiency and run-thebank (RTB) fixes to meet the deadlines set. FX operations leaders dread the recurring annual paradox of being asked to further reduce costs whilst not introducing any additional operational risk(s).

With this backdrop the FX businesses are required to provide FX services to an external client base and ‘internal’ customers who are becoming increasingly demanding whilst margins are being eroded though competition and regulation. FX activity by banks is still being closely monitored by regulators following previous FX fixing scandals (in 2015 the Financial Times reported that six banks were fined $5.6bn for the rigging of FX markets). If the interest rate market is seen as a precedent for the threat of law suits, following the impact of ‘rigging’ FX rates (used as a reference point for countless business transactions) the cost provisions for banks only increases. Once you consider the threat to the traditional franchise by challenger banks with ‘agile greenfield’ operations, the landscape begins to become cloudy for what was seen by many as a relatively low-touch, vanilla and highly commoditised market.

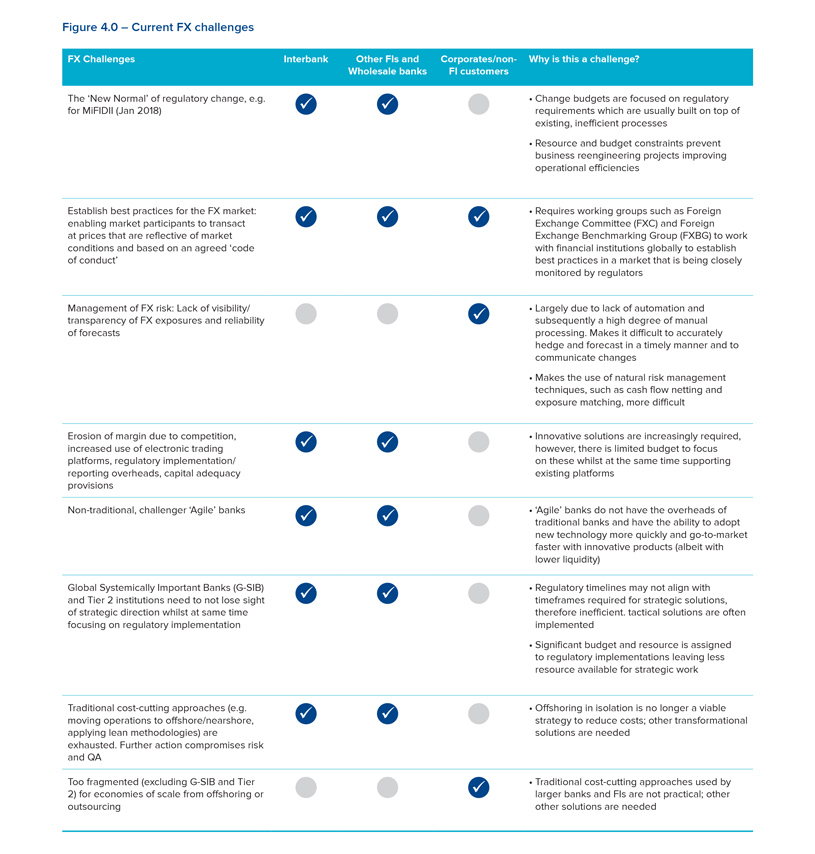

If we consider the current challenges for participants in the FX markets, they can be categorised according to three types of institutions: Inter-bank business, wholesale and other financial institutions, corporates and other nonfinancial customers. Each of these participant groups have some of the same challenges, but not all, and some are affected more than others. These challenges can be categorised into themes around: regulatory changes, establishing best practice, the management of FX risk, operational efficiency and technological challenger innovation.

The vast majority of tickets are processed through CLS. However, this does not equate to the majority of gross-traded value. Currencies supported by CLS enjoy safe settlement on a PvP basis, netting prior to settlement and a swap facility between members allowing for a >70% reduction in funding requirements. There is also a trade aggregation service (enabling long and short trades to be collapsed into fewer tickets) reducing the warehousing of transactions, and reducing points of failure, safe in the knowledge that funds will not be released until the contra side is also received into CLS.

Then there is the non-CLS-enabled market representing the remaining balance of tickets not enjoying any of the above, aside from on a bi-lateral basis with each counterparty. It is this sector which for some, represents the vast majority of the operational and risk cost. This sector of the market has multiple points of failure, with each of those points representing operational risk.

Mutualisation Positive Trends And The MSP Attraction

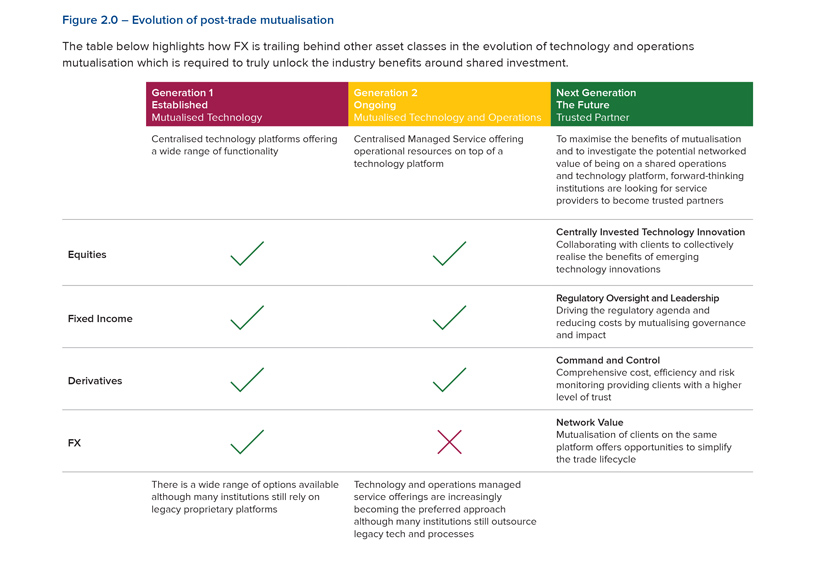

There is much to be gained from standardising for mutual benefit and this has been borne out through the introduction of SWIFT messaging standards; Cheque clearing/Link network (UK domestic but everyone signed up); APACS/ VocaLink and CLS itself. Mutualisation delivers scale and common efficient processing which reduces cost, as we are beginning to see in the equities and fixed income areas within capital markets.

In line with this, the general consensus is that there is no strategic differentiation or competitive advantage from owning back office processing. This is where the power of the MSP provider adds the additional cost benefit ‘kicker’ when both mutualisation and outsourcing are combined onto a single proposition.

The traditional offshoring based on ‘Lift and Drop’ of legacy platforms still requires run the bank (RTB) IT support. The lift and drop approach that many firms adopted meant weak processes were moved to low-cost locations but were still weak processes. Often the offshore location was empowered to implement small-scale efficiency gains – Lean Sigma etc. but did not tackle the legacy estate. Operations “cannot offshore any more – it is now a technology challenge” is a mantra often echoed by operations managers across the FX market.

■ Imagine if there was an opportunity for the FX sector to operate on a single processing platform (MSP) enabling the donor institutions to concentrate on business strategy as opposed to run the bank (RTB) activity.

■ Imagine stripping away the typical causes of ‘breaks’ and ‘unmatched’ trades preventing settlement of billions of dollars of currency every day.

■ Imagine not having to navigate the legions of late payment operators scattered across the correspondent banking network trying to establish who was responsible for not releasing a payment and incurring a ‘late payment fee’.

■ Imagine not having to call the client to explain why they did not receive their funds and having to make good the value.

All of these problems currently occur every day and are eating away at the small margins in FX trades – one ex Head of Trading has estimated margins as low as $5 per $1,000,000 traded!

The benefit of a standardised processing model will be a more efficient post-trade process via a centralised but appropriately segregated operations utility with efficient matching and exception detection and resolution. Late fee operations would be potentially eliminated with a central point of matching. In addition to this, the RTB costs reduce over time, leading to increased margins due to legacy estate decommissioning.

As mentioned, banks have been and will continue to focus on regulatory reform implementation, often requiring largescale changes to legacy infrastructure. In conjunction with this, significant change is looming on the horizon with the increased momentum of crypto-currency, technology innovation and revisions to traditional real time gross settlement (RTGS) to enable wider access and crossoperability with emerging technology. An example of this focus is a recent consultation paper published by the Bank of England on the new RTGS service for sterling, touching on all of the above. Banks are already looking at this wave of potential change. However, when it comes to trading with each other, there is a real attraction in mutualising a platform in order to concentrate in-house resources towards the FX market and payments platforms of the future.

Mutualisation Challenges

| Challenges |

Impacts and opportunities |

| Referential data |

Securing accurate and timely proprietary data (reference data, market data, transaction data) is of fundamental importance and data quality is intrinsically linked with the efficiency of operations services. One of the most critical functions for an FX managed service will be to establish a robust industry leading data governance model which is able to meet quality, timeliness, security and regulatory standards through the use of Service Level Agreements (SLAs). |

| Transparency and control |

Being able to offer transparency of service performance is crucial both for the donor organisation and the service provider. Highly flexible and analytical ‘Command and Control’ dashboards, focused on efficiency and cost per trade models, should provide a platform upon which a strong governance model can be built and regulatory control maintained.

Performance Review Boards and Service Level Agreements can be tracked and used to drive out a programme of continuous efficiency improvements.

|

| Continuous efficiency and machine learning |

Command and control analytics can be used to highlight where efficiency investment is required, but often the business case for investment in efficiency measures and technology for machine learning and robotics process automation is difficult to make within an individual organisation or department. The critical mass commercial model underpinning a managed service will enable investment in cutting-edge technologies to address efficiency barriers.

The nature of FX operations is one of continuous change through client booking models and regulation. Organisations which do not continually invest in efficiency will slowly be overwhelmed by this.

|

| Impact of distributed ledger |

The advance of distributed ledger technology is both a challenge and an opportunity for an FX operations managed service.

The challenge is clearly that we are soon to enter a period of fundamental technology disruption which will impact currency flows and challenge traditional FX processes and participants.

But the opportunity is realised through a shared investment model where the managed service provider (MSP) can start to drive consensus and establish the thought leadership and technical expertise to actually speed up the establishment of technology innovation whilst lowering the level of disruption.

|

| Integration Services and Target Operating Models |

Embarking on a migration of both technology and operations for a set of FX processes that are mission critical is a process prone to risk. Many projects and initiatives fail at this point through poor integration services and test management. The key is not to make assumptions – only by performing a top down Target Operating Model assessment can the real challenges and opportunities be assessed and planned. Once the outcome and journey is clear, it becomes far easier to establish strong governance controls and quality assurance processes. |

| Segregation of duties between front and back office |

It is critical to establish effective segregation of duties and hand-off points with the donor organisations and also establish data privacy controls between banks represented by the MSP.

The definition of roles can be challenging as each organisation has different ideas of scope and describes itself using its own personal lexicon of terms.

It is vital that these differences are understood up front and the Target Operating Model is used to gain consensus on Process Activity Task Models and Data Governance definitions.

|

| Retention of culture |

This is often overlooked, but retaining the ‘culture’ of the donor organisation is critical in order to act as a ‘gel’ in touch points between organisations.

Ensuring high levels of cultural retention both during the initiation phase and on an ongoing basis will be critical to the success of a managed service.

|

| Location of MSP/disaster recovery |

There are many factors that will influence the location of operations expertise and also the location of data and infrastructure. These factors can be both cost and regulatory driven. Another specific influencing factor especially pertinent to FX will be an organisation’s disaster recovery plans.

The key though is accepting that these factors will change over time – so the focus needs to be around flexibility. The Target Operating Model definition needs to consider these factors and also define up-front processes for managing location change to enable operations to run as smoothly as possible.

|

| Regulatory change |

All banks are facing the challenge of how to keep up with regulatory change and it is clear that this challenge is going to grow and increasingly eat into budgets previously allocated to maintaining FX operations efficiency rates. The critical mass commercial model offered by a managed service will allow this load to be shared as regulatory analysis and investment is undertaken once for all entities. Looking ahead, organisations within the managed service will be able to view regulation as a differentiator as they will have more resources available to identify opportunities within regulatory change, and also a stronger ‘voice’ on the regulatory committees. |

Operating Priorities for a Managed Service Provider Model in a Symbiotic Relationship

Whereas the attractions of mutualisation are evident, the challenges require robust debate. Decision makers within banks are pre-occupied with regulatory reforms and their implementation and have little appetite for operating models perceived to be risky and ‘game-changing’. They are already fearful of falling foul of making the wrong decision.

There will be an onus on the MSP to demonstrate the quality of its governance model and the robustness of its SLAs, as well as the viability of its technology and operating model to support multi-bank delivery that aligns to the business goals of each participant firm.

Conclusion

To tackle the challenges laid out in this white paper, GFT and Broadridge have established a working group with the remit to formulate a framework for how this type of service will evolve and to consult with interested parties who are facing the challenges articulated above.

Our belief is that these challenges are resolvable and, with enough critical mass, there are real opportunities for a wholesale change in the way FX trades are processed, to build upon and take to the next stage what has already been achieved by CLS.

In the same way that the advent of CLS was a transformational pillar in the evolution of the FX market, paving the way for increases in volume, participants and risk mitigation, a centralised and mutualised operations model, covering CLS and non-CLS transactions, could empower transformation aimed at the inefficiencies and costly FX operational model.

The motivations for institutions to seriously consider FX operations mutualisation has reached a tipping point due to the influence of the three key pressure points:

■ Unacceptably low ROE

■ The increasing cost of regulatory compliance

■ The strategic cost of technology disruption

The efficiency and cost changes that institutions have already made just to keep up have played out and the diminishing returns achieved by tactical change has resulted in organisations being backed into a corner with mutualisation the only realistic next step.

Providing our collective expertise in both operational model redesign and as a managed service provider, GFT and Broadridge together provide insight and methodology that can help shape ‘the next frontier of FX operations.’ Figure 6.0 demonstrates a draft Proposed Functional Model of how this new operational model may work.

View a full list of references for this white paper.