To understand how capital markets firms are dealing with this challenge and opportunity, Broadridge and Greenwich Associates surveyed executives at capital markets firms to learn more about their strategies to grow revenues while improving efficiency. We found firms are still grappling with the costs and challenges of regulatory compliance and legacy systems. They believe that new technologies will drive opportunities for new sources of revenue and cost savings, but they are concerned that they do not have sufficient resources and expertise to realize the potential of these opportunities.

In these dialogues, executives talked about three new technologies in particular that are driving change:

1. Cloud Computing

which provides the opportunity to reduce costs, increase speed, and improve client experience.

2. Artificial Intelligence (AI)

machine learning and robotics, which can enable firms to further automate and evolve middle- and back-office processes.

3. Distributed Ledger Technology (DLT)

which has the potential to be a unique disruptor of current business processes, revolutionizing everything from stock exchanges to proxy voting.

As capital markets businesses grapple with continuing sub-par returns on equity, there are strong opportunities to leverage these technologies to improve their businesses. In many cases, a partnership approach to non-differentiating functions can enable institutions to accelerate their ability to take advantage of the biggest technological advances in a generation, freeing up mindshare and investment to stand out from the competition where differentiation matters, and putting themselves on a stronger pathway to profit.

Capital Markets Opportunities and Challenges

Capital markets firms have undertaken massive programs since the global financial crisis to improve their return on equity (ROE), with specific focus on cutting costs — exceeding more than $40 billion in cost savings to date.1 Rising interest rates, improving economic prospects and rising profits are giving banks room to invest in new technologies. Compared to prior periods, there is significantly more optimism about future growth. Still, capital markets businesses are performing below their cost of capital. They are also competing fiercely for fees and customers, while facing growing pressure from digitization and electronification of key asset classes.

There are bright spots. Banks globally are benefitting from the trend of rising interest rates that began after the U.S. presidential election, sending profits from lending and corporate earnings higher.2 In the United States, there could be potential easing of certain regulations (for example, the Volcker rule) although the extent and timing remains unclear. U.S. banks may also soon benefit from legislation to lower taxes. Despite this, challenges remain. In Europe and Asia, there is uncertainty related to the impact of Brexit and more regulations are on the horizon that will impact global firms’ operating models. In the United States, most of the significant post-crisis regulations are expected to remain in place. Globally, the obstacles posed by new technologies, including fintech disruptors, are expanding relentlessly.

The hurdle facing capital markets firms is perhaps best illustrated by their flagging returns-on-equity. Overall, ROEs declined from 12% to 8% in 2016. ROE for the top 10 banks remained at 5% in 2016, but rebounded to 7% in the first half of 2017, with European institutions facing greater pressure.3 Having already cut staff to improve their ROE, many banks do not have the resource muscle to lead change initiatives. Overall, after 10 years of change, the industry has yet to reach a sustainable growth model, and investment analysts believe it will remain difficult for capital markets firms to beat their cost of equity capital over the next five years. A recent McKinsey report concluded that “Global banking is delicately perched between profit and loss, and the next move seems likely to be downward with the main questions being around timing and how quickly the industry can adjust."4

Technology Is Key

Last year, Broadridge surveyed more than 150 buy- and sellside equity analysts covering capital markets. That research revealed that banks had taken great strides to improve their business model and performance, but more aggressive action was needed.5 Discussions with c-suite executives and middle managers since then confirm that imperative persists. But they see significant potential promise for a step-change forward, based on the use of three transformational new technologies: 1) Cloud computing, 2) Artificial intelligence, machine learning and robotics technology, and 3) Distributed Ledger Technology (aka blockchain).

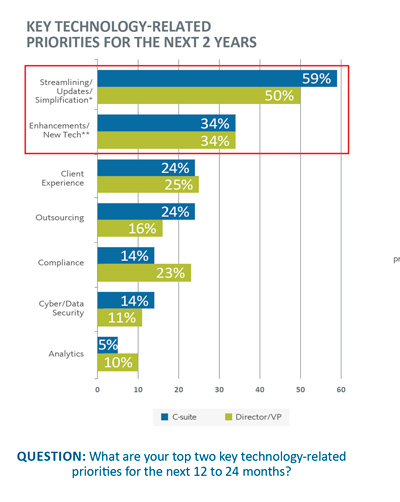

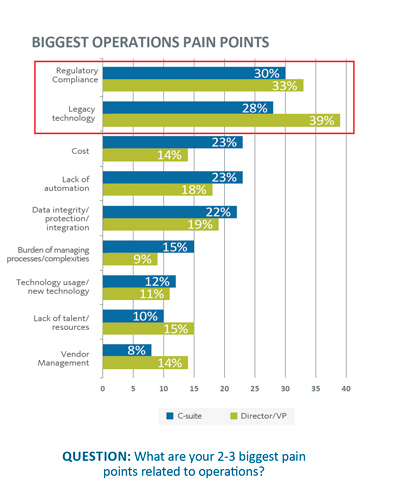

How is the industry responding? To find out, Broadridge and Greenwich Associates conducted new research, surveying key executives at 69 capital markets firms. According to these senior executives, the top priorities for capital markets firms are increasing revenues, capturing savings, and improving efficiency. Regulatory compliance and dealing with legacy systems are the biggest operational pain points that require investment. With regards to technology, their focus is on streamlining and updating existing capabilities as well as simplifying processes and enhancing operational efficiency, including working with partners to update or replace their current legacy applications. As part of this focus, executives also believe that better understanding and leverage of their internal customer data will significantly improve marketing and sales opportunities as well as the client experience. However, while firms assess how to grow their business using new technologies, they complain of insufficient resources and expertise to deal with this critical challenge.6

Industry executives agree that technology transformation will be a key driver for returning to attractive business returns. For capital markets firms, this means:

- Focusing on simplifying complex, legacy technology, especially for the largest players

- Increasing use of industry utilities or key industry partners who can mutualize costs and capabilities for non-differentiating functions

- Accelerating adoption of new technologies to cut costs, simplify operating models, and drive innovation

Looking at the current landscape, capital markets firms are adopting cloud technology at different paces, depending on the business application/function and also by the size and complexity of each firm. Artificial intelligence, machine learning and robotics will have a tangible impact on the industry within three years, and early adopters are already making investments in this area. Some observers believe that artificial intelligence could yield significant cost benefits through productivity gains of between 20-30% in units processing trades.7 Though blockchain’s transformative solutions may take longer to fully bear fruit, many firms, including Broadridge, are working on proofs-of-concept and, more recently, production-ready applications. Capturing the promise of these new technologies requires a major investment by capital markets firms. But if banks do it themselves, they must invest significant financial and human capital in new platforms while continuing to have the cost burden of operating legacy systems.

Mutualizing Non-Differentiating Functions

Since the global financial crisis, banks have already targeted most of the low-hanging fruit within their own cost structures, significantly reducing or outsourcing positions. According to Coalition Analytics, the top 10 investment banks cut jobs within their fixed income, currency, commodities (FICC) and equity Asia trading units by 22% between 2010 and 2015.8 Now they need to find other solutions, including technology innovation, mutualization to drive operational efficiencies, and changes to market structure.

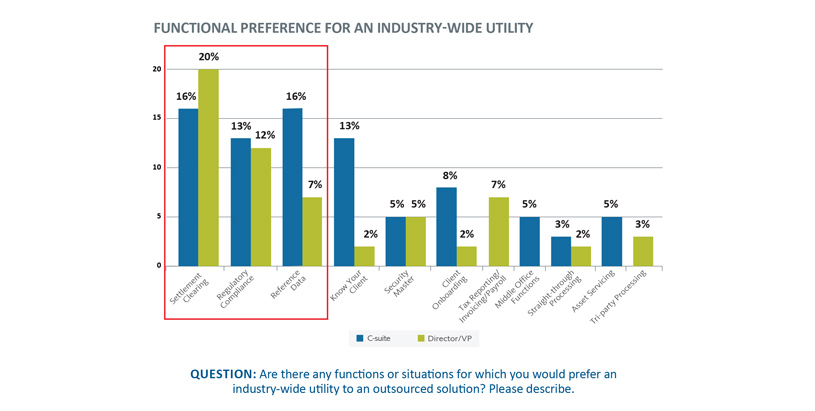

Despite this need, many capital markets firms don’t have the funding ability or intellectual capital to make these investments alone. Given the imperative to cut costs and the opportunities offered by new technologies, many institutions are now actively seeking to embrace partners who can provide an on-ramp and a shared investment model to leverage the potential of new technologies for non-differentiating functions. Among c-suite executives, 64% favor an industry-wide utility over building their own bespoke, outsourced solution.9 These executives believe that a shared approach is the best vehicle to provide such functions as settlement clearing, regulatory compliance, and reference data.

Broadridge research suggests that $2 billion to $4 billion of that could be eliminated through mutualization.10 Indeed, based on this logic, a number of leading institutions participated in multiple efforts over the past two years to form a new trade processing utility.

Despite the strong supporting logic, these broad multi-institution efforts have not been successful to date. Discussions with industry leaders point to three primary challenges:

- The inability of the largest banks to agree on their top priorities

- The lack of an available next-generation, multi-tenant global technology platform

- The high cost of on-boarding institutions onto such a platform once it is created

Three things are changing this landscape for the better. First, the realization that a phased approach makes more sense. Trying to do too much with too many institutions at the same time greatly complicates coming to agreement and significantly increases risk. In particular, commercial industry partners are able to use their balance sheet to solve one client’s challenge now, knowing that they can bring that solution to others later. This enables a brick-by-brick approach that reduces cost and risk for everyone while also significantly easing the challenges associated with on-boarding.

Second, the landscape is improved by the increased availability of the right next-generation, multi-tenant technology platform. Broadridge’s Global Post Trade Management (GPTM) platform is one such example. Now live with multiple clients, it creates a true global, multi-asset capability that previously didn’t exist in the market. For instance, one leading institution is combining more than six regional and individual asset class platforms into one integrated global platform using this technology.

Third is the need to apply next-generation technologies including cloud, AI, machine-learning, and robotics. Firms pursuing a mutualized approach can tap into intellectual capital and shared investment to drive these technologies.

Based on this approach, smart firms are leveraging key fintech partners to mutualize non-differentiating tasks and processes, from post-trade processing to compliance functions, providing cost savings and improved client experience without the challenge of standalone investments. Firms are identifying opportunities especially where utility scale and capabilities already exist, and they are working with partners to develop new utility scale solutions. This also offers firms the opportunity to consolidate technology vendors, working with key strategic partners on a global basis to achieve scale and cost savings while realizing their innovation goals.

Partnering to Innovate

Capital markets firms are increasingly focusing internal technology efforts on things that genuinely differentiate their firms from the competition. They are leveraging partnerships to add innovation in areas where they lack expertise or scale, or to enable them to focus the expertise they do have on their most differentiating areas. Four examples show how partnerships can accelerate innovation and adoption of new technology.

1. Speeding Adoption of Cloud Infrastructure

Nearly every large institution is now engaged in a full-scale effort to move large portions of their infrastructure to the cloud. These efforts involve hundreds of applications. Re-factoring applications to take full advantage of cloud capabilities is a major work effort. Leveraging third-party software-as-a-service (SaaS) providers can address significant portions of this challenge by offloading parts of the application portfolio where strong third-party solutions exist.

2. Leveraging AI, machine learning, and robotics

Scale is a significant accelerator to most effectively make use of these new technologies, which are inherently data-driven. Having access to the greatest number of use cases and volume of exceptions significantly speeds the learning and quality of solutions. Partners that see transactions across multiple clients for a given function can apply this technology more quickly and deeply.

3. Driving Distributed Ledger Technology adoption

DLT skills are in short supply, and DLT inherently requires multiple institutions to agree on an approach. Third-party partners can help in both regards. Digital Assets Holdings’ work with the Australian Securities Exchange (ASX) and with The Depository Trust & Clearing Corporation (DTCC) are strong examples, as is Broadridge’s work with JP Morgan, Santander, and Northern Trust in global proxy.

4. Creating New Network Effects

Beyond pure application of new technology, working with industry partners can drive new networks that bring value to all participants. New examples include collateral optimization, speeding securities settlement to T+1 for interested parties, new modes to trade illiquid fixed-income securities, and improved efficiencies in resolving open items driven by fails. These advances are taking shape and have the potential to create significant benefits.

These examples and others show how partnering with fintech providers that have scale, capability, and intellectual capital can provide an effective on-ramp to innovation, enabling leading firms to accelerate their efforts, focus their resources, and realize new sources of value.

Pathways to Profit.

Leading capital markets firms continue to be challenged to drive attractive returns on equity. Firms have aggressively addressed the levers available within their four walls and now need a mutualized approach to make further progress. New technology increases the imperative but also can add strain to scarce investment budgets and intellectual capital.

Mutualized approaches can drive significant benefit but in some cases have proven challenging to put into practice. Three new changes are improving this dynamic:

- The realization that banks can mitigate risk and disruption by migrating to new solutions/capabilities in a phased approach. The industry’s leaders understand that third-party technology partners can invest once for the benefit of many

- The availability of new global, multi-asset technology platforms

- An understanding that the promise of next-generation technologies such as cloud computing, AI/machine learning and DLT can be accelerated by leveraging a partnership or mutualized approach

As banks grapple with low returns on equity, executives are scrupulously assessing what they do best and what is best left to others. Working with the right partners through the coming years of technology transformation will be a key lever for driving profitable growth. Rationalizing legacy technology and driving the adoption of cloud computing, AI/machine learning, and DLT can be accelerated by using mutualized platforms for non-differentiating functions. By adopting a partnership approach to take advantage of the biggest technological advances in a generation, banks can free themselves to work on standing out from the competition, putting themselves on a stronger pathway to profit.

View a full list of references for this white paper. Opens in new window(PDF KB)