Close

Access the latest news, analysis and trends impacting your business.

Explore our insights by topic:

Additional Broadridge resource:

View our Contact Us page for additional information.

Our representatives and specialists are ready with the solutions you need to advance your business.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |

Your sales rep submission has been received. One of our sales representatives will contact you soon.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |

What does the future state of operations look like for asset managers and what are the steps that should be taken to get there?

The asset management market faces new challenges every day, including fee compression, product complexity and market expansion. To overcome them, and support the continued evolution of the industry, they will need to transform their operations. Simply improving the steps in certain processes will not be enough. Firms must work collectively to streamline requirements, eliminate steps and embrace innovation for genuine transformation.

In this white paper, the Asset Management Group of SIFMA, along with Broadridge and other industry thought leaders, explore the topic of transformation and offer their vision for the future of operations.

The pain of the global financial crisis, and the subsequent regulations, is starting to fade from view. The asset management industry is now at a crucial juncture, facing new challenges that will transform the business. In active management, the industry has created more complex products to generate alpha, while the growth of passive management, spurred by fintech competition, is compressing fees. At the same time, expansion into new markets has added costs. Now, redesigning operations is critical to being nimble enough to support the industry’s evolution. There’s also the promise of new technologies that can be used for innovation in-house and with the help of partners. Facing these challenges and leveraging these opportunities will require serious improvements to back- and middle-office operations. Everything from data validation to trade reconciliation will need to be overhauled. For genuine transformation, experts say, it’s not enough to improve the steps in a process; financial institutions need to eliminate steps. Specifically, executive members of the Asset Management Group of the Securities Industry and Financial Markets Association (SIFMA) say that leading firms should:

After nearly a decade of restructuring and regulatory challenges (and as much as $40 billion in cost cutting1), the financial services industry has advanced. But for asset managers, it’s been an evolution of incremental change rather than a revolution. Now the asset management industry is in the midst of a secular downward trend2 of squeezed fees driven by technological disruption and client demand for reduced-fee products. The result has been margin compression, increased competition, the rise of passive investing and the proliferation of low-cost products, such as exchange-traded funds. In active management, the proliferation of more complex products to generate alpha has made redesigning operations critical to creating an environment nimble enough to support the industry’s evolution. In addition, the extension of firms into new geographic markets has added costs. Those pressures have prompted consolidation, including the mergers of Aberdeen Asset Management with Standard Life3 and Janus Capital Group with Henderson Group4. Executives expect that trend to continue as part of the push to drive fund expense ratios lower.

Simplifying operational processes: For genuine transformation, experts say, it’s not enough to improve the steps in a process; financial institutions need to eliminate steps. Technologies such as distributed ledger technology have the potential to eliminate the need for certain data reconciliations.

This paper asks how asset managers can move beyond shaving more costs from such things as post-trade settlement, regulatory compliance and reconciliation. It finds that rather than seeking incremental improvements, the industry should strive to reimagine how operations are handled. Based on discussions with executives from leading asset management, buy-side and sell-side firms, as well as service providers, it assesses the drivers for change and the challenges and opportunities ahead, and discusses what actions the industry must take to reach its desired future state. The long-term vision of how middle- and back-office operations of the asset management industry should change is best summed up by one word: Simplify.

Drivers for change

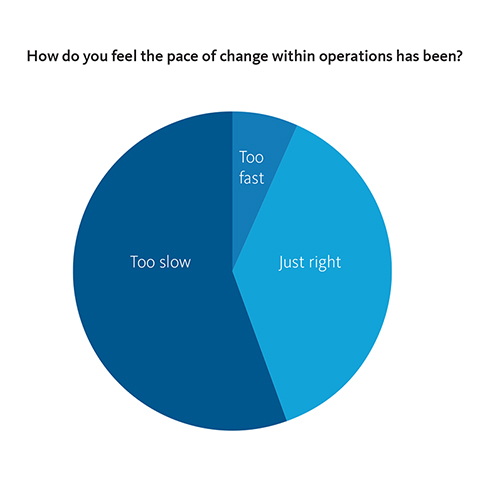

A SIFMA survey of its Asset Management Group (made up of executives from a range of asset management firms, as well as banks, insurance companies and service providers) reveals that the majority believe that the industry pace of change in the area of operations has been too slow. As famed economist John Maynard Keynes once said, “The difficulty lies not so much in developing new ideas as in escaping from old ones.”

| Answer | % | Count |

|---|---|---|

| Too slow: | 56 | 25 |

| Too fast: | 7 | 3 |

| Just right | 38 | 17 |

| Total | 100 | 45 |

The survey reveals that operations managers want to reduce operational costs for internal and external stakeholders, as well as reduce operating risks and counterparty risk. Yet they complain of working in a culture where the implementation and adoption of innovative ideas is slow, mostly because existing business models and obligations must always be considered first and systems are so interconnected. That’s understandable considering these firms must move the world’s assets around safely and securely. The old, executives explain, can never be entirely thrown out for the new, but always has to evolve, partly because of the lack of industrywide standardization of processes that at times makes the notion of more radical change seem unattainable. Executives lament, for example, that all parties in the chain—client, manager, broker and custodian—generally have their own models they view as the standard they expect to be followed.

However, demands from regulators have grown since the 2008 global financial crisis and there is an increased urgency to obtain high-quality data to streamline efforts to meet those regulations and ease the exchange of that data, both among firms and with regulators. Executives say the asset management business has struggled in the past decade to react to developments driven by both regulators and new competitors. Broadridge executive Chris Fedele says the industry has faced three significant challenges in quick succession: 1) Regulators have heaped on new rules that have required significant investment in information technology, 2) The rise of robo-advisors and efforts by fintechs to disrupt existing business models have forced many firms to play catch up and 3) The U.S. Department of Labor’s new fiduciary rule mandating that wealth managers offer the best advice at the best price has accelerated fee compression and further added to operational complexity. These three simultaneous pressures have resulted in a decade where asset managers have been reactive, rather than being able to set their own agenda for innovation.

Now it finally seems like asset management firms have a chance to work to improve their own futures. First, the regulatory environment has become more benign in the United States.

Also, three new technologies are laying the groundwork for positive change in the coming decade—cloud computing, artificial intelligence (AI) and distributed ledger technology (DLT). Cloud computing can reduce costs, increase speed and improve the client experience. AI and machine learning can enable firms to further automate and evolve middle- and back-office processes. Finally, DLT/blockchain can revolutionize everything from stock exchanges to corporate action processing. DLT could be particularly useful in operations because it can create a single “golden” source where authenticated data can be stored, updated and extracted, potentially eliminating countless processes across the industry. Having squeezed a lot of excess cost from operations in recent years, executives now want to find ways to transform.

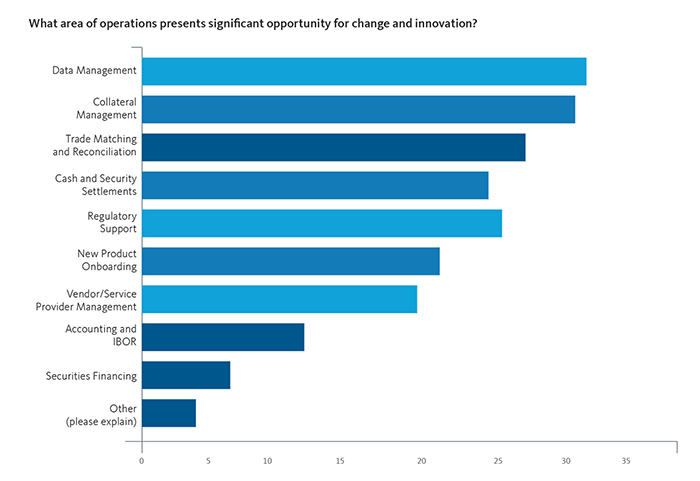

Operations managers highlight several areas where advances can be made—80% see significant opportunity for innovation in data management; 78% see potential in collateral management; 69% in trade matching and reconciliations; and 62% in cash and security settlements.

| Answer | % |

|---|---|

| Data Management | 80 |

| Collateral Management | 78 |

| Trade Matching and Reconciliations | 69 |

| Regulatory Support | 64 |

| New Product Onboarding | 53 |

| Vendor/Service Provider Management | 49 |

| Cash & Security Settlements | 62 |

| Accounting and IBOR | 29 |

| Securities Financing | 16 |

| Other (please explain): | 9 |

Derivative operations, creation of robotic processes, expense management/oversight, corporate action processing, derivative messaging.

Asked what technologies can advance those goals, 36% say continued advances in the electronic execution of derivatives or securities, 34% see promise in blockchain and 18% expect advances from AI/RPA and machine learning.

The problem with operations in asset management today is perhaps best illustrated by the fact that in the age of the smartphone, fax machines are still in use. While faxes have gone the way of the horse and buggy for most businesses, you can still find these relics of the 1980s in asset management firms where they are used to communicate trade authorization and manually review faxed signatures of instruction and authorization.5 This highlights that too often, change in operations is incremental and additive instead of leapt forward. Bureaucracy has only intensified in recent years as regulators have added a thicket of new rules.

Now, a future goal for executives running operations should be to make processes simpler and more efficient. In doing so, however, be cautious of making small, incremental changes that will soon be overtaken by more substantive change, says Eric Bernstein, President of Asset Management Solutions for Broadridge. “The challenge is not to build walls you will soon knock down,” he says. Firms should instead look to cut costs in two ways: “Are there more efficient ways to do things with new technology and can you cut explicit costs by using utilities or service providers?”

Almost uniformly, executives say a major problem with operations across the industry is the lack of standardized data. With every firm having different database input fields in their in-house systems, such routine processes as reconciliations and margin calls can be onerous. For example, for margin calls to be processed uniformly would require setting standards such as putting the client’s name in field one of a database, client account number in field two, the security CUSIP in field three and so on. In order to set the stage for process transformation, the industry must move to standardized data, executives say. Standardized, extractable data will provide a starting point to shift processes to new platforms, such as DLT. For example, the Monetary Authority of Singapore is developing a national know-your-customer (KYC) utility for financial services firms. Using digital identity software that was jointly developed by the Ministry of Finance and GovTech, the lead agency for digital and data strategy in Singapore,6 the system enables residents to give their personal data just once to the government and retrieve personal details for all subsequent online transactions with the government. The utility streamlines operations by eliminating the need for financial services firms in Singapore to maintain their own KYC records.

Amy Caruso, Director of Strategy and North America Business Development with DTCC-Euroclear GlobalCollateral, says making small, practical improvements generates what she calls operational alpha — using extra liquidity from operational improvements to boost investment performance. In many cases, being simpler means taking a bolder approach where tasks are entirely eliminated. New technologies can help that process, but getting to that long-term vision requires a change in mindset where firms become more collaborative. Today, finance works tactically when it comes to operations. Can this process be made faster? Can incremental savings be captured? Instead, what’s needed is to think strategically. Can this process be automated, or better yet, eliminated? If it can be eliminated, what must happen at the industry level, rather than the firm level, to make that happen? Only then will the industry make material changes. A case in point is trade settlement.

Shorter Settlement — Not Great, But Global

Wall Street has moved from T+3 to T+2 settlement,7 but many asset managers had wanted to go further, to T+1 or one-day settlement. South Korea already has T+1 settlement and China has same-day settlement. In the United States, same-day trading exists for certain cash products, such as repurchase agreements, futures and overnight commercial paper, so it can be done. Executives say a reason for the slow pace of change here is that the push to reach an agreement on shortened settlement came directly after the adoption of Dodd-Frank, leaving many with little appetite for radical change. Joseph Haddock, Managing Director and Head of Business Operations at Annaly Capital Management, says the industry was well-prepared for the U.S. move to T+2 and that the timeline was likely overly cautious. He hopes the T+2 transition will be leveraged to further shorten settlement cycles.

Some want faster or instant settlement because it frees up capital for sell-side firms while buy-side firms would enjoy reduced counterparty and market risk. Others believe just getting to T+2 was important because it brought the United States in line with global standards. That’s important because 82% of firms say their business is now global, while only 18% say their business model is domestic only. DTCC’s Caruso says T+2 was the right step. “If you run before you walk, you trip, and in the financial markets, if you trip, that hurts Main Street and Wall Street,” she says. “ Having moved to T+2, the industry can work on moving to T+1”.

|

Settlement ties up capital and could be done faster. |

Improving operations will require firms to take the initiative to collaborate on industry-wide solutions for common problems. That will ultimately boost wealth generation for clients — a win-win for everyone. “Since 2008, Wall Street has not fully gained back the trust of Main Street,” says Jesse Robinson, Managing Director of Investment Operations for State Street Global Advisors. He believes that if the industry makes bold investments to improve in areas to reduce risk and support lower-cost structures for clients, trust will be restored. He favors a radical approach to overhauling operations by making “material change.” How can the industry reduce costs materially through a new, simpler model that will allow clients to preserve or generate wealth much more efficiently? “We should be disrupting and reinventing ourselves before somebody else does,” Robinson says.

Clients benefit from operational improvements, too: Faster, better, nimbler and less costly asset management operational processes result in client benefits, including improved reporting, access to more diverse products and lower fees.

Getting to a future state where operations are significantly more efficient will require short- and medium-term actions from every firm:

Short-term: The industry must 1) leverage what it already does well, 2) use tools that allow better collaboration and that facilitate interoperability between firms to eliminate common processes, 3) work with utilities and shared service providers to support new shared services, standards and utility models, 4) develop common platforms to standardize workflows on non-differentiating processes and 5) establish incentives for firms to work well together.

Medium-term: The industry must 1) embrace new technologies from cloud computing and AI to DLT/blockchain, 2) look outside for industry service partners or utilities to share costs and risks and develop products faster. Additionally, 3) each firm should look at what processes can be eliminated or automated by applying new solutions that can be universally applied across the industry rather than making incremental advances within a single firm.

A big driver of medium-term change will be new technologies. AI/RPA is already heavily used in operations, but executives say it can go significantly further. For example, if identifying exceptions in trades has been automated, the next challenge is to set parameters for resolving those exceptions without the need for human intervention. Executives say the biggest impediment to making the maximum use of AI/RPA is the lack of standardized data.

The full scope of processes DLT can change remains unclear, but leading financial institutions are piloting programs that imagine what that future might look like. JPMorgan Chase, for example, is building a blockchain on the crypto-network Ethereum that could digitize contracts to improve the review of loan originations and streamline the legal review process during underwriting.8 Digital Asset Holdings has partnered with the Australian Securities Exchange (ASX) to prototype a DLT system that could replace its current clearing and settlement platform.9

Collaboration

Executives say that a crucial cultural change that asset managers need to undertake is to understand that when it comes to non-differentiating functions, sharing common systems makes sense. That can mean using the services of a utility or service provider, such as Broadridge for proxy communications or DTCC for settlement, or investing in a common platform that negates the need to maintain an in-house bespoke system.

Operations executives say blockchain, along with the use of standard identifiers, could make dealing with regulators easier. Some wonder whether compliance could become “self-service,” with regulators accessing information stored on the blockchain to negate the need to prepare reports. Others say that a “golden” source of data that is standardized, and therefore easily extractable, could make fulfilling new demands from regulators much easier and remove significant costs. Using a central portal to clear these operationally difficult transactions successfully can speed settlement. And analytics identify the root cause of operational breaks to solve problems at the source. Using similar approaches to solving more common problems, executives say, would leave them more time to focus on developing systems to set their investment teams and portfolio managers apart from the competition.

Getting to this future state will require:

Exactly what form that collaboration should take remains subject to debate. Some executives would like firms to come together at the highest levels. Others feel change driven by middle managers can engender improvements. Some see advances occurring in smaller increments.

At one end of the spectrum is the notion of a leaders’ forum—a sort of G7 or G20 for Wall Street—charged with setting a bold, mutually beneficial vision for the entire industry. In the past, Wall Street has come together to do such things as forming DTCC to solve the paperwork crisis that paralyzed the financial industry in the late 1960s or working on the implementation of new rules to support compliance associated with Dodd-Frank after the financial crisis. Now the industry must move beyond tactical collaborations that solve a single problem, instead building a culture based on a shared strategic view of the future. Such committees could tackle big-picture issues, such as promoting the use of central counterparty clearinghouses or breaking down legal barriers and impediments that are by-products of regulations.

Some executives say that the industry should leverage associations such as SIFMA to gather players across verticals, from broker-dealers to investment banks. Within each vertical, representatives of the leading firms should come up with their top specific pain points and solutions to solve them, leveraging service providers as needed to develop those fixes. That type of work is already underway in some areas. For example, leaders from the Futures Industry Association and SIFMA AMG have been meeting to discuss problems that clearinghouses and exchanges, futures commission merchants, investment managers and administrators are having with exchange-traded derivatives and OTC-cleared workflows. The goal is to find common challenges and then learn from each other to either leverage the best practices among firms to develop an industry standard or find processes that can be standardized to alleviate pain points. To date, the meetings have highlighted three common problems: 1) trade confirmations of exchange-traded derivatives are antiquated and not standardized, causing difficulties in reconciliation, 2) updates of commission and fee schedules are not centralized, resulting in stakeholders using databases and spreadsheets that might not be up-to-date and 3) the communication of margin calls is not standardized. Executives at those meetings say that solving these problems will build trust among stakeholders so they can tackle issues that might be more controversial in the future. At the same time, executives say stakeholders have to keep an eye on what is needed in the next three-, five- and 10-year time frames and work collaboratively toward their goals. Executives need to think big but take small steps to get the industry moving toward these goals. They note that any substantive discussions about transforming the industry should include presentations from regulators and customers so that their needs are incorporated early in the process.

Broadridge’s Bernstein says a great example of past collaboration that produced substantial change is the Financial Information eXchange (FIX) protocol,10 which began in the early 1990s as a communications platform between Fidelity Investments and Salomon Brothers but became the global standard for trade communication and straight-through processing in global equity markets. The change, made in 1998, was not incremental but occurred over time, shifting information that had been disseminated from human to human by phone to an electronic platform that eliminated errors. Within a decade, the FIX protocol, which standardized how trades were conducted, was being used uniformly.

Executives say cultural changes must start within firms, setting incentives for executives to change and improve operations processes. Without firms displaying a clear appreciation of the costs and benefits of changes, many middle managers will feel that by making improvements they are merely working themselves out of a job. To combat that, firms should invest in human capital, rewarding staff that improve processes with training in IT skills, offering learning in such things as automation, systems interaction and data structure.

Overhauling operations has risks that firms need to work to mitigate. Among those risks is losing specialized knowledge as operations are automated, so firms must strive to retain subjectmatter expertise amid change. Asset managers should also be aware that automation can cause unintended consequences. A great example of that was the Flash Crash of 2010, when the stock market briefly fell by 10% as a result of an automated algorithmic trade that was programmed to take account of trading volume, rather than price or time, and was executed in 20 minutes instead of over the course of several hours.11 Given that risk, as more processes are automated, firms must be on alert for such conflicts and work to thwart them by learning from issues as they arise. Toward that end, firms can look to other sectors, such as the nuclear power industry, to discern best practices on how to deal with the proliferation of automated processes. A cultural risk at many firms is being overly concerned about earnings this quarter and this year, rather than focusing on what will happen if investments are not made now in technologies needed three, five or 10 years from now. Balancing those competing needs is crucial to long-term success.

Finally, Tim Cameron, the Head of SIFMA’s Asset Management Group, says, “As the industry incorporates new technologies, the number one risk is from cyberattack—something that firms must protect against as they create new platforms and systems.”

From the days of the ticker tape to being able to trade stocks on a mobile phone app, Wall Street has a great history of innovation. With Google, Apple, Uber and an army of fintech startups ready to disrupt the world of finance, now is the time for Wall Street to take a fresh look at how operations are done and to completely reimagine back- and middle-office functions to serve the industry for the next 30 years. The goal is to simplify everything and, where possible, eliminate functions and processes entirely. As myriad tasks are eliminated, that may reduce the number of back-office functions. However, this sea change will produce more middle-office roles for workers charged with transforming processes, undertaking change management, business analysis and developing new ways of working in the future. This requires a cultural change of realizing the difference between what makes a firm special and drives investment performance and what should be standardized. Firms do not generate exceptional returns by having bespoke messaging systems and reconciliation workflows, so such things should be standardized to trim costs and allow effort to focus on boosting investment performance. When the industry reaches its future state, the nomenclature “operations” itself should cease to exist. The end result will be a Wall Street that is less transaction-based and more thoughtful and analytical, and an asset management business that is set to thrive for another generation.

View a full list of references for this white paper.