Close

Access the latest news, analysis and trends impacting your business.

Explore our insights by topic:

Additional Broadridge resource:

View our Contact Us page for additional information.

Our representatives and specialists are ready with the solutions you need to advance your business.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |

Your sales rep submission has been received. One of our sales representatives will contact you soon.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |

![]()

More than 30 years ago, Yale University’s endowment fund began to move investment assets out of marketable securities and into what were then little-known asset classes that collectively became known as “alternatives.” Since then, other institutional investors—and, more recently, growing numbers of retail investors as well—have sought to replicate the success of that model by allocating steadily increasing amounts of assets to alternative asset classes. That shift accelerated dramatically in the decade since the Global Financial Crisis as investors recognized the diversification and other benefits that alternatives can provide, and sought out new, uncorrelated sources of yield during a period of historically low interest rates.

Just 15 years ago, alternative asset classes made up only 6% of the global investable market. That share is expected to grow to 24% by 2025, according to the Chartered Alternative Investment Analyst Association.1

The rapid growth of alternatives is putting buy-side operations teams under stress. In the world of alternative investments, a lack of public, standardized data combines with complex and heterogenous deal structures to make operations a challenge. The unique characteristics of alternative assets create a heavy load of manual and bespoke work demands. Those demands start with setting up the investments in asset managers’ systems and extend into reconciliation, reporting, payments and a host of other essential operational functions. As Ron Withelder, Managing Director and Operations Manager at J.P. Morgan Asset Management explains, “For alternatives, you need everything you need for public assets, but at a much more complex level.”

Complicating the picture even further is the fact that the operational demands vary, both across alternative asset classes—say from private equity and hedge funds to real assets and private credit—and within individual asset classes, with many deals and funds containing customized terms and structures created to meet the needs of participants. This variation makes it difficult, and sometimes impossible, to centralize and streamline operational processes. For that reason, many operational functions are still conducted manually—a situation that increases costs and introduces a level of human risk that is not present in public liquid assets.

Investors and other market participants are working hard to create efficiencies and alleviate the pressure on operations teams. They are standardizing operational functions where they can and applying technology to automate processes to the fullest extent possible. However, to support allocations at current scale, the industry will have to go much farther. It will need to develop new models and solutions that simplify operational functions, reducing costs and resource requirements.

But as alternatives continue to expand, the industry will have to accept that change will come only incrementally. “When it comes to alternative operations, there is no silver bullet,” says John Partenza, Vice President of Product Management for Broadridge.

There is no universal definition of alternative asset classes. Although there is some broad agreement that assets like private equity and hedge funds belong in the alternatives category, there is no comprehensive taxonomy of assets accepted by the industry. An asset class like private debt might fall into the alternatives bucket at one firm and the fixed-income sleeve at another.

However, based on our conversations with SIFMA AMG members and market participants we have assembled a working definition that includes asset classes most commonly categorized as alternatives. For our discussion of operations, we will consider the following asset classes as alternatives:

The term “alternatives” encompasses a wide variety of assets. The differences among these assets are so large that some of the professionals interviewed for this report balk at the term “alternatives operations” altogether. It is more useful, they say, to simply discuss the operational requirements associated with individual asset classes, as opposed to trying to artificially combine them under a single label.

While there is truth to that contention, the broad “alternatives” designation plays an important organizational role for investment firms, many of which structure their operations functions to include an alternatives team tasked with supporting all asset classes that fall outside the scope of standard operational processes and infrastructures designed for public and liquid assets.

Firms choose this type of structure because they understand that, despite differences, many of the asset classes grouped into the alternative category share a common set of traits and requirements. Meeting the operational challenges associated with these unique characteristics requires specialized expertise and dedicated resources.

The Ops Team: The Source of All Data

One of the main things these asset classes have in common is that, unlike traditional asset classes, they have no public, centralized source of data. As a result, one of the most fundamental and important responsibilities for an alternative operations team is capturing basic and essential deal data. “You are the data source,” explains Broadridge’s John Partenza in speaking to the challenges of private debt. “You, the deal team, the borrower and the documents—that’s where the deal data comes from. There is no other source.”

For every alternatives investment and transaction, the operations team must review the paperwork that documents the agreement, including legal documentation, term sheets and partnership agreements. Working closely with the legal team, operations professionals scour these documents carefully, line-by-line, extracting the information the organization will need to identify, execute and support the transaction throughout its lifecycle. “Control-F is your best friend,” says one operations professional, describing the hours his team spends pouring over documents.

Several professionals interviewed for this article say their firms are experimenting with optical readers and other technology that they hope will one day be able to capture much of this information for them. To date they’ve found only limited success with the most structured of the documents, meaning that for the foreseeable future their teams will continue reading through every line of deal documentation.

As they comb through these materials, operations teams are looking to extract details like the name of the entity or entities, the investment series, the amount of the investment, the lockup period, and all the events and data they will need to manage and monitor over the lifecycle of the fund or investment.

It’s a cumbersome process. “It’s so inefficient that you have to wonder how they have been able to monitor their deals to this point,” says one industry professional.

One of the biggest secrets of alternative asset classes is the surprising number of errors investors receive in reports and communications from their asset managers and general partners. With alternatives now making up a meaningful share of portfolio assets, those error rates are becoming more consequential. One operations professional says worries about omitting essential data are what keep him up at night. “It’s the unknown,” he says. “The things we might miss.”

Operations Throughout the Lifecycle

With basic data extracted and entered into the system, the operations team takes over the management of the entire investment lifecycle. Although operational processes vary considerably from asset class to asset class, most alternatives share the additional following operational requirements:

Automation Advancing Among the Most Liquid Alternatives

Although alternatives operations pose many unique challenges, the industry is light-years ahead of where it was just a few years ago when it comes to processing and settling some alternatives transactions.

Alternative assets exist on a spectrum. The closer you are to the more liquid and standardized end of that spectrum, the more closely the trade lifecycle and associated operational requirements resemble those of public markets.

For the last decade, buy-side and sell-side firms and other market participants have been working to build systems that make trade processing, reporting and settlement more efficient for the most liquid alternatives, including non-traded REITs and certain business development companies, hedge funds, private equity funds, and other assets. One of the centerpieces of this effort is The Depository Trust & Clearing Corporation’s (DTCC) Alternative Investment Product Services (AIP) platform. AIP is a standardized, centralized platform that automates core operational processes to compress cycle times, enhance transparency, and minimize errors and risks. Through this platform, DTCC processes some 50 million transactions per year (the majority of which are investor position and activity reporting), and has issued unique identifiers for more than 8,000 alternatives funds.

“We’re not all the way there, but we’ve made significant progress,” says Justin Schwartz, Executive Director, Product Management for AIP at DTCC.

In the world of alternatives, operational tasks are often much more difficult and time-consuming than they would be with a public asset.

For example, with a public investment determining a valuation for the asset is as easy as logging onto a Bloomberg terminal. For private investments, determining fair-market valuation is a manual and subjective process managed by a specialized in-house valuation team or third-party vendor. Reporting is also a much more complicated task. In alternatives, operations teams frequently need to dive back into paper deal documentation to obtain data requested or required by clients and regulators. The operations team must also keep up with changes in reporting requirements by updating their data collection and reporting processes—a task that requires significantly more work in a manual, paper-based setting than within a more standardized, digital framework.

These operational demands are often large enough to affect the economics of an investment. If firms could eliminate or even minimize these additional requirements, “the overall cost structure would go down,” Broadridge’s John Partenza says.

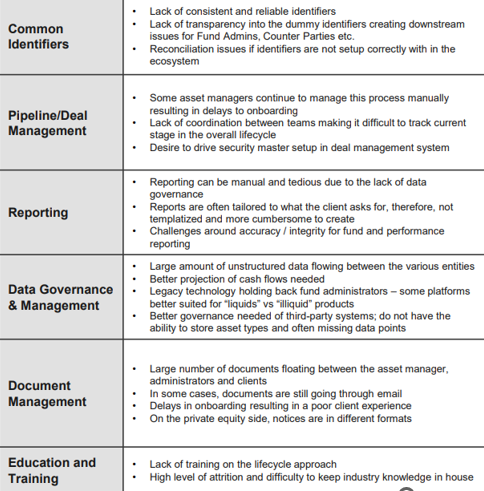

Chart below shows the most common operational challenges posed by alternative asset classes, as identified in a recent study commissioned by SIFMA’s Asset Management Group and conducted by Sia Partners, a global management consulting firm.

Common Operational Challenges for Alternative Asset Classes

Although alternative investments share some common operational demands, every alternative asset class presents its own unique operational headaches. Here are some examples of operational challenges associated with individual alternative asset classes:

Private Equity: In private equity, investors commit capital at the point of investment, but that capital is deployed only when the general partner issues a capital call. Operations teams must monitor and manage that process through the life of the investment. For an investor taking on the role of a limited partner in a private equity fund, the internal operations team must track capital commitments and calls, and then, within each capital call the team must monitor how the GP is allocating those funds between management fees and investments. Operations teams will also have to process any distributions from the GP and categorize them as gains on investment or returns of capital for use in performance calculations and tax reporting. The operations team of the LP will also sometime be tasked with monitoring the portfolio companies into which the GP is investing. Although the GP will provide its own reporting, an asset manager acting as an LP in a fund has an obligation to report to its own investors, and as such will often do its own monitoring.

Hedge Funds: Hedge funds—especially institutional funds—offer the benefit of established fund structures and, usually professional administration. These characteristics have created at least limited opportunities for investors to standardize certain operational functions. In recent years, however, the boundaries between hedge fund and private equity strategies have begun to blur. New hybrid funds are hedge funds in name, but their investments and investment structures more closely resemble private equity. So too do their operational demands.

Private Debt: In public credit markets, covenants are spelled out in plain terms in the standardized loan documentation. From there, it’s easy for operations professionals or automated systems to capture the covenants and establish required monitoring procedures. In private markets, those covenants can be listed in deal documentation, legal documents, emails or other places. At times, terms might have been agreed over a handshake and not included in any of the deal paperwork. If the operations team is not effectively monitoring all that information, the firm can miss out on real economic impact, such as covenants that would alter deal terms in the event of changes in interest rates or missed fee payments.

Commodities/Real Estate/Hard Assets: In hedge funds and private equity, investors are generally dealing with professional-level administrators. That’s not necessarily the case in other alternative asset classes like real estate, commodities and hard assets. In these asset classes, an investor might find herself dealing with the GPs and LPs of an oilfield in Texas who are not in tune with the day-to-day management of an investment.

As environmental, social and governance standards gain prominence in investment markets, operations teams will have to be involved in capturing and reporting ESG information from alternative asset classes. There is no one else to do it. In Europe, asset managers are already asking deal teams for expansive ESG information on deals and portfolios. In alternative asset classes, those deal teams are turning to their partners in operations for data sourcing and monitoring. Obtaining ESG information will require operations teams to scour legal documents, GP and LP financial statements and “anything else you can get your hands on,” says Jennifer Harris, Vice President in Operations at J.P. Morgan Asset Management.

There is no standard organizational structure for alternative operations. Because of the heterogenous nature of the operational requirements and the bespoke nature of operational solutions, every firm approaches alt ops from a slightly different perspective. That perspective is based on their unique organizational structures and cultures, and the specific alternative asset classes they use.

Operations professionals do agree on one thing: The time to consider operational requirements is before entering any alternative asset class. Investment companies tend focus most of their attention on deals, deal terms and economics. “How deals are managed and operated is usually a secondary concern,” says Broadridge’s John Partenza. “That leaves it up to operations teams to figure out how to manage the deal.”

Most firms start by comparing an alternative asset to a comparable asset in public markets and looking for similarities, or areas where the firm can use processes from the public side to create efficiencies in operations supporting the alternatives. Some functions required to support alternative investments cannot be automated and must be completed manually. The best way for an operations team to manage these demands is to create an electronic checklist of all the manual tasks that need to be completed daily, weekly, monthly or at other intervals and set up reminders to both the person assigned the task, and the back-ups who will perform that role when the primary is out.

The Portfolio Operations Group

For most firms, the basic organizational unit for supporting alternative investments is the portfolio operations team. These teams, usually composed of just a few individuals, are responsible for managing the operations of alternative investments and supporting alternative investment teams. Typically, the professionals making up those teams come from the finance group. Often, they have a special affinity for data and technology. They combine this expertise with their finance backgrounds and knowledge of strategies and products to understand alternative operations workflows and determine how data can be purposed for investment teams, investor relations, fund investors, firm leadership and all other constituencies. “It’s the combination of finance and operations; the definition of Fin-Ops,” says Jonathan Broch, Executive Director of Lionpoint Group, a consultancy to alternatives investors and advisors.

The portfolio operations group typically sits between finance, investor relations and investments. Its primary role is to structure and manage data—typically from a single alternative strategy—and make those data available to all three of those groups. Portfolio operations teams, which typically report into the CFO, often with dotted line reporting to the investment teams, standardize KPIs and financial reporting for the underlying asset within their strategies, and also have responsibilities for core tasks like analytics and valuations. This is a key function, and one that is sometimes missed by newcomers to alternatives when building out their operational structures. “The portfolio operations team is the glue between functions and maintains the golden copy of investment data for the firm. In the absence of this function, departments resort to tracking data in their own silos in an incomplete or inconsistent manner, leading to a plethora of data and reporting challenges,” says Jonathan Broch.

Specialize in the Middle Office, Standardize Everything Else

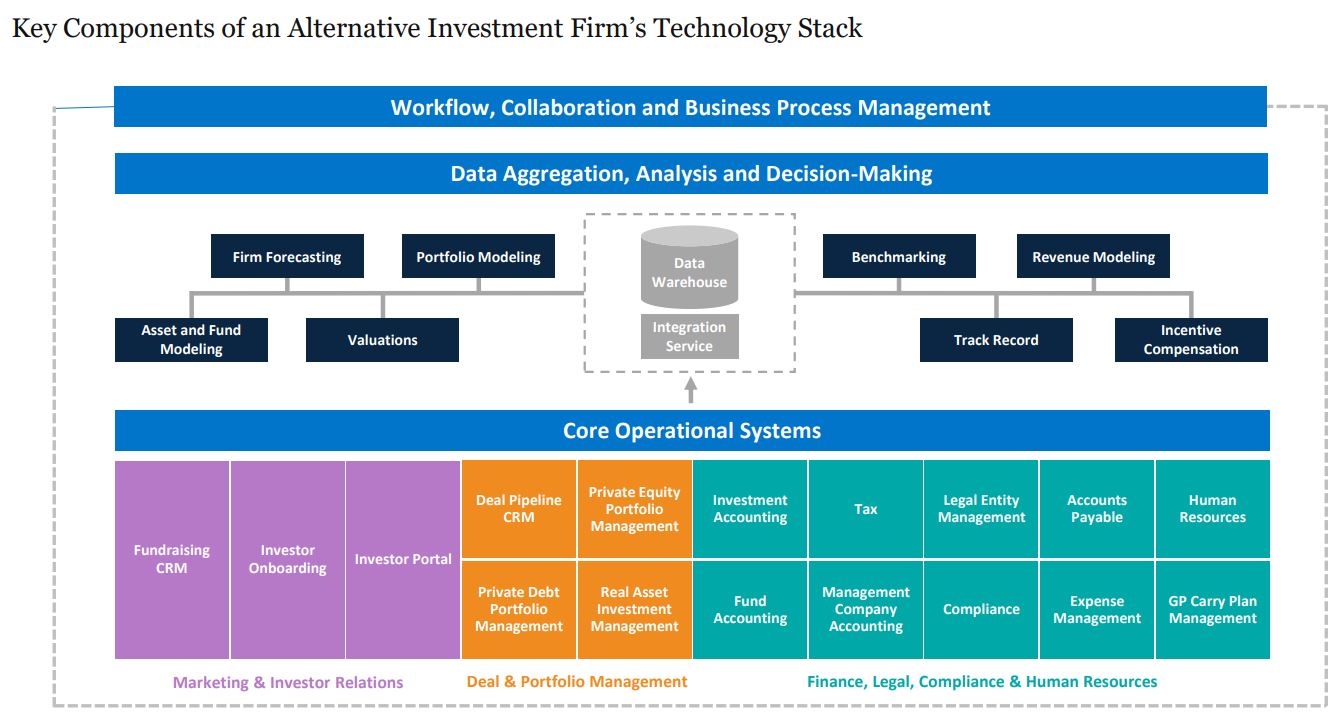

Looking at the broader organization, many firms follow a common strategy: Build out the middle office with highly specialized teams composed of professionals with niche expertise in individual asset classes, while integrating everything else to the fullest possible extent. That everything else includes core operations, client service, data management, fee management and performance, and investor reporting. This strategy also applies to underlying technology systems: In the middle office, alternative products like private equity often require their own technology systems, with specific features and functions based on the unique characteristics of the asset class.

Chart below illustrates a standard technology infrastructure architecture for alternatives operations. Although exact configurations will vary from firm to firm, most investors employ the same basic blueprint. At the bottom of the technology stack are a series of core systems that form the base layer of the operational platform. On top of that base layer sits the organization’s data management system or data lake. Within or alongside the base layer are a series of applications or platforms that support highly specialized functions like valuations, forecasting or modeling. “Organizations initially focus on building efficiencies through the adoption of core systems for specific business functions, but it is important to have a clear vision and strategy for how everything connects together” says Lionpoint Group’s Jonathan Broch.

Source: Lionpoint Group

In a tight labor market, finding the specialized talent needed to staff alternative operations teams can be a daunting task. Operations managers say it’s particularly hard to find the right talent for the middle office, which requires expertise in the nuances of individual alternative products.

As Aruna Parthiban, Vice President in Asset Management Operations at Goldman Sachs Asset Management, explains, because operational processes are bespoke and manual, “operations professionals must understand the entire front-to-back workflow, and be aware of the upstream and downstream impacts of any action.” And because many alternatives operations professionals work on more than one asset class, they must develop this level of knowledge for each one.

Even experienced operations professionals can struggle when first introduced to alternatives. “Not many people have the specific asset class knowledge that’s required,” says J.P. Morgan Asset Management’s Jennifer Harris. “It’s a very small pool of people who actually know this stuff.”

Today, It might be even harder to keep that talent once you have it. “For the last year we’ve been getting robbed of people and talent,” says an operations professional who says his firm is losing operations talent to hedge funds, boutique managers and larger asset management organizations who are increasing their presence in alternatives.

The fundamental challenge in alternative operations is a lack of standardization. Diverse deal structures and datasets that are incomplete and incompatible create the need for bespoke operational processes and systems, which increase complexity and cost. As a result, any progress in standardizing alternative assets has the potential to unlock huge savings.

Making deals and deal documentation more consistent would make life easier for operations professionals and lower operational costs for organizations. For example, using consistent fee structures, or sticking to the same interest payment periods and calendars on private loans can reduce the burden on operations teams. Even if deals can’t be entirely standardized, organizations can create templates they can use for various scenarios, rather than remaking the process from scratch every time. For example, a firm might have three main schedules for loan repayments, and deal teams pick one.

There are many opportunities to apply that type of standardization. For example, operations teams for large funds of funds receive capital call notices from literally thousands of private equity firms. “Every one is different,” says Cameron Boice, Managing Director at Goldman Sachs Asset Management. Every manager has its own language and every notice has its own structure. These differences make it difficult if not impossible to automate the process, meaning that operations professionals have to read and manually enter the information into the firm’s systems. The same holds true for investor onboarding, subscriptions, LP stake transfers and many other tasks.

Similar inefficiencies exist throughout the industry. Eliminating them will require industrywide cooperation. Several initiatives are already in progress, including efforts from DTCC, SIFMA, IPA and the Institutional Limited Partners Association (ILPA). All these groups are working to make alternatives easier to buy, sell and manage by establishing common data and reporting standards.

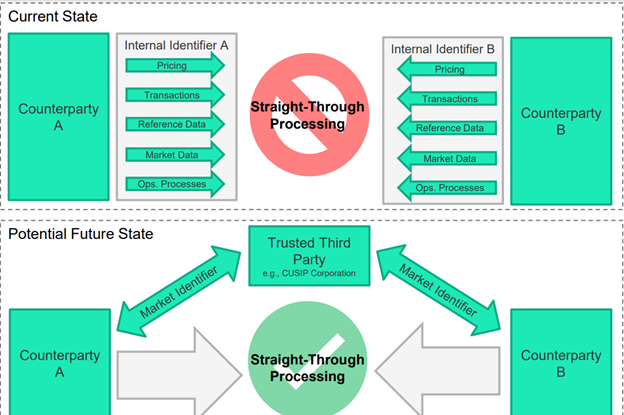

Common Identifiers

One of the most basic challenges these and other groups are working to address is the lack of common identifiers for alternative assets. The absence of these identifiers is one of the main causes of operational inefficiency. “It’s hard to match a trade or agree on a position without a commonly used identifier,” says one operations professional. “The lack of standard identifiers creates operational challenges and introduces real risks and new costs to money settlements.”

Chart below illustrates how the widespread adoption of a common identifier could transform alternatives operations by enabling seamless communication among counterparties and other market participants, and laying the foundation for straight-through processing.

Common Identifiers: The Critical Missing Link to Straight-Through Processing

Source: Alternative Operations Assessment, Conducted by Sia Partners for SIFMA AMG.

There are options available to issuers looking to obtain an identifier for their fund or security. For example, CUSIPS are easily obtained for relatively small start-up and renewal fees. DTCC’s AIP also offers security identifiers that can be used for alternative funds.

However, private issuers often see little benefit in obtaining an identifier. To the contrary, many issuers and investors see deal privacy as one of the most important benefits and a primary driver of alpha. Obinna Nwankwo, Managing Director and Director of Private Investment Services at Wellington Management suggests one easy step the industry should take to make some incremental progress on the issue: create some mechanism that informs companies about the potential benefits of obtaining an identifier when they first file for incorporation. Those benefits—in the form of greater visibility to the investment community while your company is private—could be substantial.

The industry is working on more comprehensive solutions. Several industry groups are trying to rally support for new common identifiers. Some investors are adopting IDs from third-party technology vendors that can serve the role of common identifiers. Joanne HansonBonney, Managing Director at Ares Management, says her firm was able to achieve real efficiency gains through automation after adopting an industry solution for private loans—a move that has dramatically reduced her team’s workload from notifications. In the past, it would take her team weeks to manually process loan notifications at the end of every quarter. Today, the firm uses the solution for all loan notices. Not only does this reduce the operational burden and lower overhead costs, it also “reduces error rates by orders of magnitude,” she says. “This really moved the needle for me and my team,” she says.

Looking ahead, Bharat Sawhney, Partner in the Wealth and Asset Management Practice at management consultancy Sia Partners, says the industry should work to create new solutions that can address the issue of data fragmentation without disclosing important private data about individual deals. He suggests a model in which an established third party like CUSIP provides a permission-controlled identifier in which issuers have complete control over which details are visible and to whom.

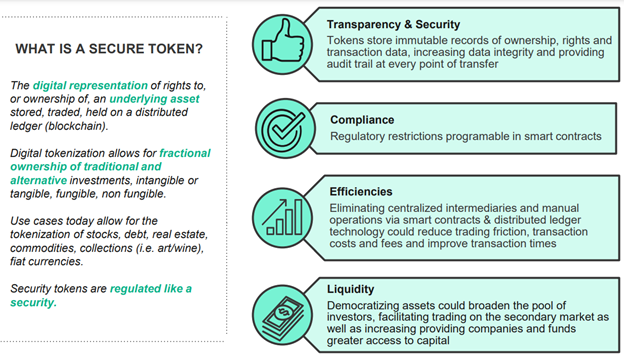

Market participants are also experimenting with more creative approaches, like applying FpML, the open-source protocol used to share information on derivatives. Some operations professionals express enthusiasm about another, even more innovative technology: tokenization. The graphic below shows how tokenization is being applied in both public and private investment markets.

Source: Sia Partners

While all these ideas are still in the nascent stage, the rapid growth of alternatives could accelerate the drive toward standardization and common identifiers. “To me, there has to be some standardization for this velocity of business to keep up,” Sawhney says. “ROI is a big piece of this,” says one operations professional, who notes that until the business starts to scale, standardization requires big investments with limited payoff. Momentum for common standards and identifiers could get a further boost from the growth of alternative assets in retirement plans, which, in addition to expanding scale, could potentially increase attention from regulators.

Standardization: Pros and Cons

Of course, not everyone agrees that standardizing alternative assets should be a top priority. Lionpoint Group’s Jonathan Broch sees limits to how much benefit can be achieved through standardization. “Investments in alternatives have so many nuances with regards to how deals are structured and what KPIs are important. While some level standardization is eventually inevitable, there is just too much fragmentation in the market to communicate the narrative of alternative investments in a standard fashion” he says, noting that individual firms have created their own internal systems for identifying assets and managing data. Even if a standard identifier was available tomorrow, it wouldn’t eliminate the other major data-related challenges faced by investors in alternatives, he says. Although the industry would certainly benefit from standardization from an efficiency perspective, Wellington’s Obinna Nwankwo notes that the lack of transparency is also a key value driver for the industry. “Opacity, the lack of public information, is a feature of alternatives that people find attractive,” he notes.

In many ways, all the operational challenges associated with alternatives operations can be traced back to data management. For that reason, establishing a well-designed, enterprise data governance model is an essential first step to revamping alternatives operations and achieving real efficiency gains in alternatives or any other asset class.

In private assets, every investment brings a unique set of data that needs to be located, processed, integrated into the operations process, and finally aggregated into the firm’s broader financial reporting systems. It’s a fragmented universe of disparate data sources, all using different standards and formats.

“Whoever creates the Bloomberg for alternatives will be twice as rich as Mike Bloomberg,” says Wellington’s Obinna Nwankwo.

Overall, asset managers do a good job collecting data from alternative transactions at the product level. The real challenge kicks in when it comes time to integrate those data into the larger organizational data management framework. Most firms have introduced at least some form of strategic data management across all asset classes—including alternatives. At the most basic level, most firms have created standardized fields and formats that capture the basic features of transactions. In an ideal world, this data would flow into a central data lake where it can be distributed to and accessed by all downstream systems and teams, ensuring data consistency and timeliness and dramatically reducing the amount of time it takes to create and deliver client reports.

Not all investors have reached that level of data sophistication. But almost all are moving in that direction. Until very recently, alternatives just weren’t big enough for most firms to warrant a full-fledged data integration effort. That’s changing as alternatives grow as a share of asset management AUM. “Some asset managers have kind of just left alternatives off to the side because they were never big enough,” says J.P. Morgan Asset Management’s Ron Withelder. “Now you must integrate.”

Sound Data Management Pays Off

Clients that achieve strong information flows with cleaner sets of data do a much better job at staying on top of regular daily and weekly tasks like reconciliation and closing the books, and are much better positioned to be able to respond to unscheduled queries and events with timely and accurate information. In addition, organizations that have moved to this more efficient end of the spectrum can expect to experience the benefits of reduced costs and could eventually be able to reduce the size of their operations teams. That’s especially the case for firms with data robust enough to feed sophisticated artificial intelligence and machine learning platforms. “Building good data management processes internally is the best thing you can do in an environment with so much variability,” says Broadridge’s John Partenza.

Alternative operations are lightyears ahead of where they were a decade ago thanks to technology. Whereas operations professionals throughout organizations once tracked key data on their own spreadsheets, today systems connect functions like treasury and cash management, allowing teams to share at least some level of standardized data.

The first technology designed specifically for alternative asset operations hit the market in the late 1990s. These early applications mainly targeted fund accounting. As allocations to alternatives increased in the early 2000s, investors began allocating significant resources to private market operations. That funding attracted new entrants, who came to market with systems designed to support additional functions such as fund raising, investor relations, and the investment function. In that period, the ultimate goal of many vendors and investors was the development of a comprehensive system for managing the full lifecycle of an alternative investment, similar to the increasingly end-to-end OMS systems used in public equities.

That thinking started to change in the 2010s, in part due to technology innovations like the cloud, software as a service SaaS, and APIs, which together made it much easier to “plug and play” separate applications into an organization’s technology platform to perform specific tasks. The global pandemic pushed that evolution into overdrive by forcing investors and other industry participants to switch to digital systems and processes, expanding the market for third-party developers.

Today, asset managers have immense opportunities to leverage innovative technology. “Until recently, there were few vendor solutions available for alternatives,” Broadridge’s John Partenza says. “People just used old-fashioned spreadsheets and tried to leverage technology solutions not built for purpose.” The rapid technology innovation forced by the COVID-19 crisis altered that situation forever. “Today, investors are seeking out the right tool for the right job,” he says.

The interoperability of systems has allowed firms to go a la carte, and for vendors to focus on perfecting solutions for narrow functions. These trends have led to a proliferation of providers, who have come to market with upwards of 50 solutions aimed at specific alternative ops functions ranging from portfolio monitoring and CRM to investor reporting and accounting. “This is not bolting on or filling gaps,” says Goldman Sach’s Cameron Boice. Rather, these discrete systems will use APIs and other technology to create seamless connectivity that from a functional perspective delivers comprehensive front to back coverage. “It would be a holistic system that with efficiency, scale and the flexibility to meet the needs of changing products,” Boice says.

The increasing flexibility of technology platforms is also expanding opportunities to outsourcing operational functions like valuations, fund administration. Wellington’s Obinna Nwankwo says supplementing the operations team with outsourced partners in specific areas is a good way to free up their time for work that can only be done internally. “There are areas like credit agreement reviews where you just need completely bespoke processes,” he says. “Build your internal teams there.”

Even in the bespoke world of alternatives, technology is creating opportunities for investors to automate operational functions.

For most investors, the tipping point is scale. When alternative assets make up only a small portion of AUM or revenues, the ROI on challenging automation initiatives simply isn’t worth the cost and disruption. Generally, as the alternatives portfolio or business starts to grow, investors adjust to the new volumes by hiring additional employees to execute existing manual operational processes. Eventually, firms reach a point at which the existing operational infrastructure simply can’t handle the flow, or the costs and logistics of hiring new employees to expand capacity simply become unbearable. At that point, firms starting looking for select opportunities to digitize and automate. “There are no huge wins,” says J.P. Morgan Asset Management’s Ron Withelder. “You take what you have and make it as efficient and scalable as possible. That’s the job.”

As they target the lowest-hanging fruit for these efficiency enhancements, the operations function evolves into a mix of manual and automated. That’s the state most investors find themselves in in 2023. One professional interviewed for this report says her firm has created a subset of its operations team devoted to implementing intelligent automation tools. Every three to four weeks they release some technology that helps move a team from a spreadsheet to an app, or from emails into a workflow system.

There are many other examples of success. One operations professional reports that his firm has used automation to compress the time needed to create capital call notices from “a couple days to a couple hours.” Firms that once took 45 days to close their books on funds at the end of a quarter are now doing it in less than 30. Another firm has enhanced efficiencies in expense processing, and sees significant opportunities for automation in bank account opening.

Across the industry, private loans have advanced fastest in automation. Because they are able to draw on relevant experiences, processes and technology from the public loan market, market participants often make private loans their first target for digitization and automation. Investors, vendors and other market participants have made significant automation progress in real estate, where new solutions are coming to market regularly. In hedge funds and private equity funds, well-established fund structures professionalized administration have created at least limited opportunities for investors to standardize certain operational functions.

However, relative to public assets, the bespoke nature of alternative deals acts as a constant constraint. For now, firms are automating wherever they can find opportunities. “This is not reinventing the wheel,” says Broadridge’s John Partenza. “It’s just reorganizing and eliminating friction.”

The future of alternative operations will be a technology-enhanced environment in which asset managers employ a series of interoperable systems that perform specific tasks and automatically extract and share data. Plug-and-play capabilities will allow smaller firms access to the same functionality used by their bigger peers. Meanwhile, interconnectivity among systems will facilitate the data capture and management required to power predictive analytics. Data from the valuation process will flow naturally to investment teams for performance projections and fund modeling while also automatically populating systems that calculate track record and other key metrics. “This is real value creation,” says Lionpoint Group’s Jonathon Broch. “Real-time, predictive analytics give leadership insight to drive quality deal-making at higher volumes.”

The ultimate goal is an end-to-end system that delivers some level of straight-through-processing for alternatives. Given the unique characteristics and customized operations processes of individual alternative asset classes, it’s not likely that this system would come fully assembled from one vendor out of the box. Rather, any end-to-end platform for alternative operations will likely be a sophisticated amalgamation of individual systems designed to meet the needs of certain asset classes or functions. These discrete systems will use APIs and other technology to create seamless connectivity that from a functional perspective delivers comprehensive front-to-back coverage. “It would be a holistic system with efficiency, scale and the flexibility to meet the needs of changing products,” says Goldman’s Cameron Boice.

When the industry achieves or even approaches that goal, investors will be able to get NAV, performance reporting and any other information on any alternative product from the same source, in the same format at the same time. To the investor, the information flow will be seamless, with no indication that the data are coming from an underlying bespoke operations system. Importantly, this will allow the investor to self-service regular events like capital contributions, redemptions and capital calls for any asset.

In the end, some operations professionals envision a “super middle office.” In this configuration, most or all of the core operational functions outside the middle office have been centralized and standardized. In many cases they will be managed through organizational centers of excellence in which they are partially or fully automated in partnership with technology vendors. In this set-up, the middle office would exist as the central point of contact, helping the front-office solve problems and assisting in new product development, new distribution channels and vendor management. Since many of the core tasks that now occupy the time of alternative operations teams would be transferred or eliminated, these super middle offices would likely have far fewer professionals dedicated to day-to-day operations. Instead, operations teams would focus on data, spending much of their time sourcing, scrubbing and distributing data to the front office and end investors to inform decisions.

Change in alternative operations is coming slower than most professionals would want. However, there is no scenario in which the industry moves backwards.

In an industry defined by its heterogeneity, even the most sluggish, incremental steps toward digitization, standardization and automation are an accomplishment. They also represent a one-directional current. As one operations professional concludes, “Things might change faster or slower, but no one who’s using DocuSign is going to decide they want to go back to signing pieces of paper and putting them in the mail.”

Your sales rep submission has been received. One of our sales representatives will contact you soon.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |