Close

Access the latest news, analysis and trends impacting your business.

Explore our insights by topic:

Additional Broadridge resource:

View our Contact Us page for additional information.

Our representatives and specialists are ready with the solutions you need to advance your business.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |

Your sales rep submission has been received. One of our sales representatives will contact you soon.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |

Broadridge’s Martin Walker, head of product for Securities Finance and Collateral Management, and Amanda Sayers, product owner for Anetics, explore how the securities lending market would fair in a T-Instant world.

The common consensus is that there are only three states of matter; solid, liquid and gas. Heat any solid long enough and it melts into a liquid, heat it further and it eventually turns into gas. However, if you put a sufficiently large electrical discharge into a cloud of gas, such as lightning or you create an electrical arc, a fourth state of matter is produced called plasma.

Plasma can often be seen in neon lights, displays and in plasma balls. It appears gaseous, but it is unlike gases, and is indeed more similar to solids in that it is a good conductor of electricity. Steps in securities trading can also be comparable to these distinct ‘states’. Some may consider the states to consist of order creation, execution and settlement. Alternatively, it could be thought of in terms of trading, matching and settlement. As the securities settlement cycle continues to be compressed, what new and strange states are likely to emerge? And what does that mean for securities lending and borrowing?

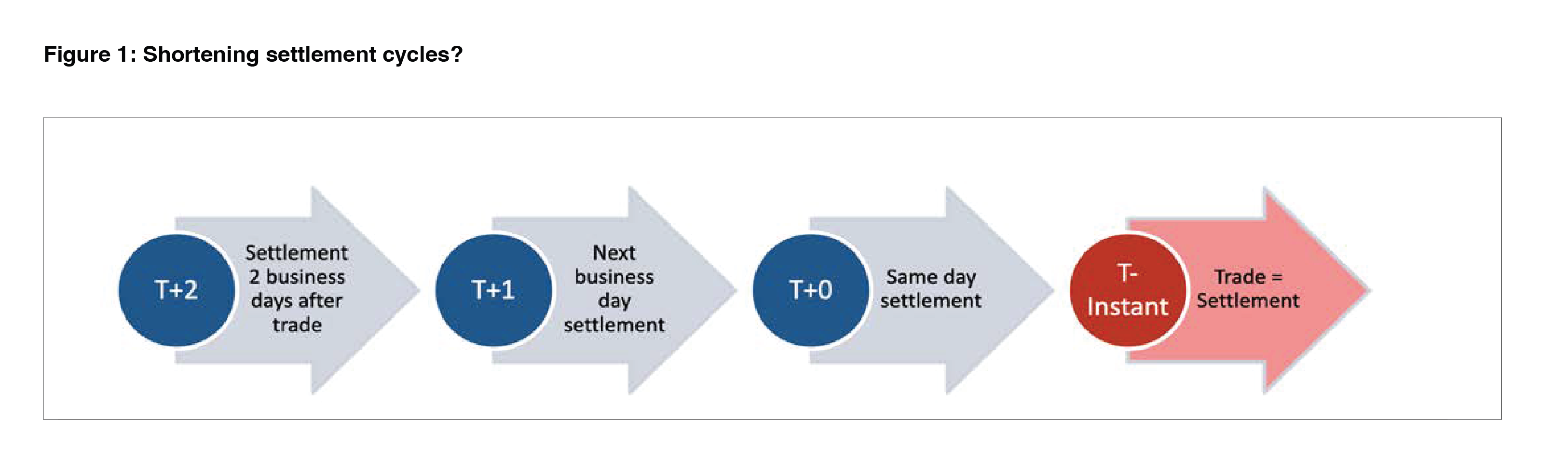

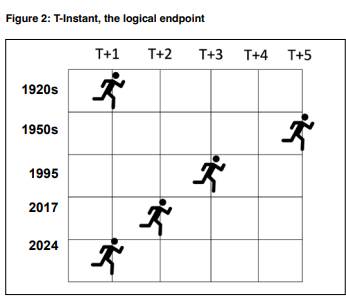

Settlement cycles exist because of the need to carry out the administrative tasks necessary to transfer ownership after the sale of a security. In the 1920s, the settlement cycle on the New York Stock Exchange was T+1, in spite of an almost entirely manual process. In other words, trades would settle one business day after a trade. In the 1950s and 1960s, the settlement cycle was increased to T+5 as manual processes could not cope with the dramatically increased volumes that ultimately led to the so-called ‘Crisis of Wall Street’.

During these decades, the back offices of broker-dealers were overwhelmed by paperwork and were therefore forced to use computers for the settlement process. Eventually, further automation and the creation of dealer-to-client (DTC) allowed the US equities settlement cycle to gradually reduce again, to T+3 in 1995 and T+2 in 2017. We will likely see the reduction to T+1 in 2024.

Figure 1: Shortening Settlement Cycles?

Securities lending has managed to survive these changes because it generally operates under a shorter settlement cycle than the cash equities market. However, with the proposed reduction in the settlement cycle to T+1, the time available for a core securities lending process and recalls will be uncomfortably squeezed by the shortening of the equities trade lifecycle.

Market participants are attempting to work through the impact of T+1 recalls. However, to be prepared for the future, it is necessary to start thinking about the logical end point of compressed settlement cycles. Not T+0 — same day settlement — but ‘T-Instant’, also known as ‘Trade = Settlement’.

Figure 2: T-Instant, the logical endpoint

T-Instant settlement refers to the execution of trades which are then settled in seconds or even milliseconds. The post-trade world is finally catching up with the high-speed world of algo trading to free up billions of dollars deposited at CCPs to mitigate settlement risk.

Trying to squeeze the settlement cycle for equity trades into an even shorter period may produce major implications for securities lending.

The time delays in the current system, in both settlements and trading, are highly advantageous for creating liquidity. Market makers can trade all day long, creating liquidity for the market, without needing physical possession of the stocks they buy and sell. As long as they flatten their position by the end of the day, the operations team will be able to settle the trades two business days later — subject to a certain amount of friction.

Those trading short in the US market can sell stocks — creating liquidity for buyers — knowing that if they have located the stock beforehand, they should be able to borrow the stock and have it delivered in time for them to settle their sale of stock. A T-Instant world means participants can only buy stocks if they have the funds in an appropriate account, and they can only sell if they have possession of the relevant stocks in a depo.

Under the pressure of instant settlement, the trade and the settlement would merge into a new state — like plasma.

A liquidity squeeze would prove challenging for anyone familiar with the way the current market works, unless there is a radical change to the trade execution process. For instance, by slowing down trading to have periodic auctions, rather than matching orders — which currently makes life difficult for short sellers.

In a T-Instant world a short seller would need to either:

Designing a market that supports the latter model is logically possible. However, it is important to discuss whether the model for doing so would be too much for the market to swallow. This model would include fixed term lending transactions, a market order book for borrows and loans, harmonised collateral (i.e. cash only) and automated exchange driven margin calls. The first two options make for a clunkier trading process for short sellers, but are still possible, despite additional costs.

The T-Instant experiment makes some of the trends that are currently nascent seem more inevitable. These include fixed terms of trades and the centralised clearing of trades. Only when these become standards can securities lending become more similar to cash equities trade, and ‘atomic transactions’ — that include the sell, borrow and their settlements — can be created. Atomic settlement makes the recall process close to irrelevant, because securities would have to be returned at the duration of the trade.

This would leave the door open for settlement failure if short positions cannot be covered by borrowers in time to return stock to lenders. In fact, if sellers are dependent on holding securities to sell, and buyers can only buy if they have funds, most causes of fails would be eliminated. This would leave securities lending as one of the main sources of settlement failure. In such a situation, it is likely that a market mechanism would be introduced that automates buy-ins for borrowers that are unable to return stock by the designated time.

T+0 may not seem quite as extreme as T-Instant. It would allow for a whole trading day to deliver stock. However, the window to recall stock, have it returned and then delivered in relation to a sell, would be small. The overall trading and settlement day is likely to be extended, with a significant proportion of settlement activity for cash trades and financing trades happening at the end of the day. If there is a massive compression of settlement activity at the end of the day, the issue lies with the further squeeze of time to borrow stock and have it delivered to cover settlement failures.

The push towards greater clearing and fixed terms for trades will not be as strong as in a T-Instant scenario, but it will still exist. If no movement is taken in that direction, there is the possibility of a greater number of settlement fails and those fails being directly attributable to stock lending. Even if those shorts are covered within the timelines set out by regulations, such as Reg SHO 204, the pressure would likely build on the industry to reduce fails. At a minimum, traders would need an accurate and real-time view of their settle positions, new trades and fails. Relying only on overnight position feeds from stock record systems would not work.

Finally, we return to the near future of T+1. System processing deadlines are being extended to allow recalls to be received and actioned until 11.59 pm (Eastern Time). The outstanding questions are whether:

No market consensus has emerged about the answer to these questions, but there are likely to be more fails. As described in the T+0 scenario, simply following existing practices should allow fails to be addressed within regulatory deadlines, but it will not present a pretty picture of the impact of securities lending to the overall market.

Coming to a consensus on market practices is essential, as is removing any frictions in trade processing. A real-time view on trading and settlement is needed to deal with potential recall situations. This real-time view should be conducted as early as possible on the trading day.

Looking beyond T+1, we will quote the movie Plan 9 from Outer Space: “Greetings, my friends! We are all interested in the future, for that is where you and I are going to spend the rest of our lives.”

This article was first published in issue 337 of the Securities Finance Times magazine.

Our representatives and specialists are ready with the solutions you need to advance your business.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |

Your sales rep submission has been received. One of our sales representatives will contact you soon.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |