Schließen

Access the latest news, analysis and trends impacting your business.

Explore our insights by topic:

The payments industry has been no stranger to various disruptions in terms of the surge in technological advancements and behavioural shifts across customer demographics. Learn more about the multi-faceted challenges bearing down on banks across Europe and why operational transformation is now a strategic imperative.

Like other industries, the payments industry has been no stranger to various disruptions in terms of the surge in technological advancements and behavioural shifts across customer demographics. With business models already being challenged, the COVID-19 pandemic has impacted the industry adversely. As trade volumes declined by more than 13% in 2020, per the World Bank estimates, the COVID-19 aftershocks pushed the payments industry to adapt to multiple trends such as the rise in card payments and the increase in contactless channels.

Meanwhile, the velocity of regulatory and other mandatory changes are adding another layer to the already complex payments landscape. Regulators are advancing the Payment Services Directive 2 (PSD2)/ open banking mandate along with the European Payment Initiative (EPI) for a unified payment solution tailored for Europe. However, banks are reluctant, owing to various risks involved in sharing data and potential hefty penalties when breaching data protection regulations. These risks, coupled with fragmented compliance activities and differences between local and regional regulatory initiatives such as PRETA or STET in Europe along with multiple systems and schemes, further exacerbate banks’ operational and financial burden. A case in point being the emergence of several real-time payment schemes globally and the lack of interoperability.

Regardless of the issues mentioned above, regulations are expected to be reinforced in the near future as various fraudulent activities act as a tipping point for regulators to ensure customer safety.

At the same time, the industry is experiencing a mass switch towards contactless payments. In April 2020, 29 European countries increased their contactless payment limits, while the demand for mobile payments doubled in some countries. In France, cards are now seen as the preferred means of payments, while in the Netherlands, instant payments are becoming the new normal. The pressure on the payment providers is to offer real-time payments services 24 hours a day, seven days a week.

However, the increase in online transaction activities such as online shopping forced by the pandemic has propelled fraudulent activities. Unfortunately, it currently appears elusive to totally eradicate the risk of fraud. Still, payment providers continue to develop sophisticated fraud prevention and detection tools to reduce the incidence through artificial intelligence (AI) and robotic process automation (RPA).

With major incumbents struggling to prioritise their short-term and medium-term goals in the current volatile, uncertain, complex and ambiguous environment (VUCA), coupled with the surge in operational costs, the payment function within the banks is gradually becoming a commodity. The cost of ownership versus the benefits is becoming inversely proportional, leading to many banks to investigate outsourcing their payments function while concentrating on their unique selling propositions.

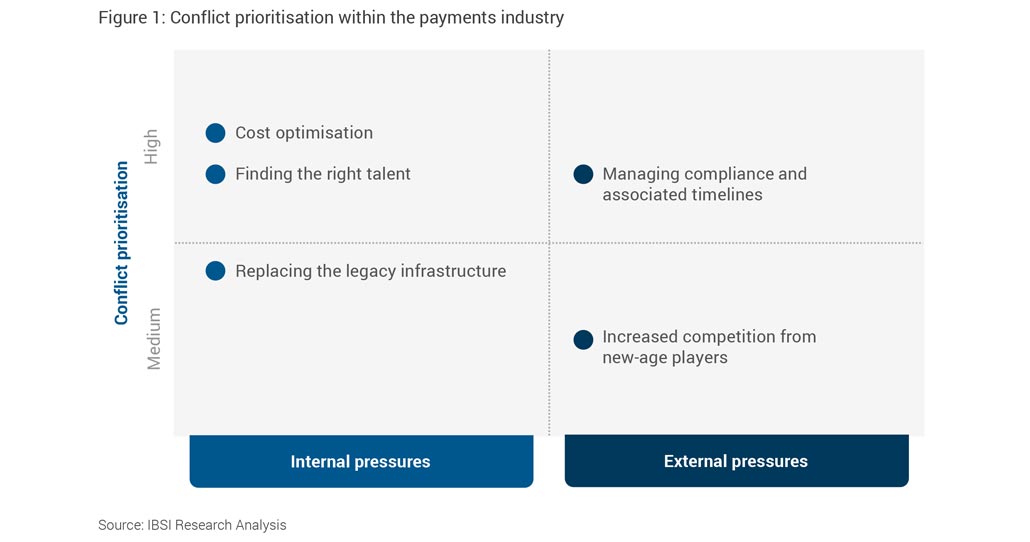

Rapid growth and colossal changes come with their own set of challenges and conflicts. When it comes to the payments industry, these conflicts affect both the incumbent banks and the overall payments ecosystem. Despite sincere efforts towards harmonisation and democratisation, the European payments system remains complicated at the moment. These headwinds and growing customer expectations have mired the industry with external and internal challenges and conflicts.

As technology, talent and time become crucial enablers, banks need to figure out a dynamic one-stop shop solution that addresses their challenges and at the same time meets the ever-changing, growing consumer expectations.

Banks and financial institutions (FIs) face numerous challenges, and a focused approach is required to confront those comprehensively. The first step is to identify the challenges, which will vary for individual FIs, and prioritise them according to business objectives.

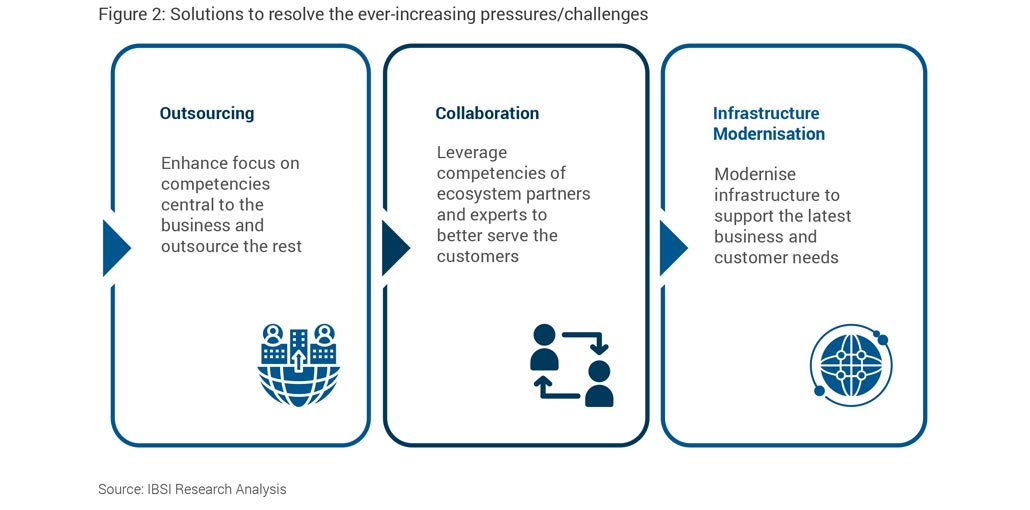

Amidst increased regulatory activity and mandatory market change, managing compliance is one of the highest priorities, especially for European FIs. Cost optimisation, fraud reduction, and attracting skilled talent are a never-ending tussle. Outsourcing and collaboration can help banks tackle these high-priority tasks.

Outsourcing and mutualised, shared services bring in a host of advantages for banks. Banks can leverage a Payments-as-a-Service (PaaS) model to access the latest technology and offer innovative services to customers without worrying about costs related to infrastructure modernisation or their current technological capabilities and competencies. PaaS platforms, supported by dedicated payment specialists, will also be better equipped to facilitate alignment with new technological developments, regulatory requirements, or new market infrastructures, and enhance the future readiness of banks. Outsourcing payments processing may also be an impactful workaround for Tier 2/Tier 3 banks to deal with any shortage of skilled resources.

Shifting to a modern, cloud-based infrastructure can enhance banks’ resilience, agility, and scalability, while also reducing the total cost of ownership (TCO) and enabling the switch to operational expenditures Amidst increased regulatory activity and mandatory market change, managing compliance is one of the highest priorities, especially for European FIs. Cost optimisation, fraud reduction, and attracting skilled talent are a never-ending tussle. Outsourcing and collaboration can help banks tackle these high-priority tasks. (OPEX) from capital expenditures (CAPEX).

Furthermore, it can also enable banks to achieve significantly higher levels of operational efficiency through best-in-class straight-through processing and the dynamic resolution of processing exceptions, and provide the scalability to grow, capture new revenue streams and enhance the quality and range of client service provision without capacity or resource constraints.

The current environment has opened opportunities for banks and payment service providers alike to reevaluate and retool many ways of doing business. Why not take this opportunity to take a hard look at the current processes and technology partners? With the right platforms, technology and talent, incumbents and payments service providers will have the confidence and support to tackle the better (and busier) days ahead.

Alastair McGill,

General Manager Data Control, Broadridge Financial Solutions

Alastair has more than 25 years’ management experience in the Technology and FinTech sectors and today leads Broadridge’s Payments and SWIFT business that serves more than a hundred clients around the world. The business has expanded rapidly and most recently announced a new Payments as a Service BPO offering for European institutions seeking to transform and modernise their payments infrastructure in response to market and regulatory changes.

Shitij Raj,

Senior Analyst, IBS Intelligence

Shitij has more than five years of experience in management consulting and global research with expertise in Payments and FinTech domain. His experience includes working with a variety of multinational and bluechip organisations in the Financial Services sector. He is a Senior Analyst at IBS Intelligence for global Financial Technology research, banking technology, supplier assessment and custom advisory services.

For more information, please contact the Broadridge team at global@broadridge.com

Your sales rep submission has been received. One of our sales representatives will contact you soon.

Want to speak with a sales representative?

| Table Heading | |

|---|---|

| +1 800 353 0103 | North America |

| +442075513000 | EMEA |

| +65 6438 1144 | APAC |