EXECUTIVE SUMMARY

Banks increasingly understand the importance of investing in improving their aging cash management systems that are too often “siloed” and rely on manual processes. In a rising interest rate environment, it is particularly important to utilize better cash management technology and practices that can optimize the value of this asset.

As banks seek to replace outdated cash management infrastructures, they are looking for a platform that can produce accurate liquidity metrics, comprehensive daily reports, an enterprise-wide view of risk and has the ability to aggregate cash across the organization. In addition, the system must be flexible and extendible so that it can respond to changing regulations.

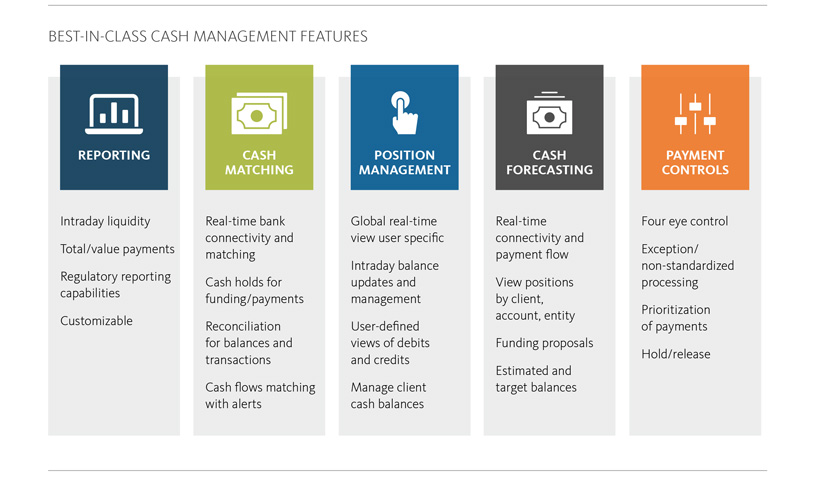

Investing in real-time technology can transform cash management from a reactive cost center into a proactive profit center. Many organizations find that buying an off-the-shelf solution from a technology vendor can produce the fastest results at the lowest price. However, any solution must be able to deliver these five capabilities—reporting, cash matching, position management, cash forecasting, and payment controls.

| A ROBUST CASH MANAGEMENT SOLUTION MUST BE ABLE TO DELIVER THESE FIVE CAPABILITIES |

| 1. Reporting |

| 2. Cash matching |

| 3. Position management |

| 4. Cash forecasting |

| 5. Payment controls |

INTRODUCTION

Historically banks have under-invested in cash management systems. Before the 2008 global financial crisis when margins were strong, there was little incentive to optimize cash management. After the crisis, banks needed to focus on complying with new regulations and improving middle- and front-office efficiencies to boost lackluster returns. As a result, investments in cash management took a back seat. However, as many banks still struggle to produce returns on equity above their cost of capital, cash management technology and practices are being reexamined.

In the intervening years, global businesses have become increasingly interconnected and, therefore, cash management has grown ever more complex. This is reflected in the number of relationships maintained by global banks. According to PwC, the average large bank deals with eight core banks plus 21 additional banks and maintains 344 bank accounts with local banks (“Nostro accounts”).1 Handling so many relationships and currencies makes monitoring, managing and controlling activities extremely challenging.

Many organizations are unable to track the cash passing through all of their accounts in real-time or forecast balances accurately. Moreover, they cannot hedge effectively or meet their regulatory and compliance requirements. Ultimately, these shortcomings result in increased risk and suboptimal decision-making.

As the final stage of the transaction cycle, cash management often ends up relying on disparate systems that produce inconsistent and untimely data. In addition, data latency and the manual nature of these processes result in manual errors, struggles with data collection and mapping, and regulatory reporting issues. The nature of the challenge is highlighted by the fact that 86% of systems in use today for cash management use spreadsheets for cash forecasting.2

“86% of cash management systems in use today use spreadsheets for cash forecasting.”

CHALLENGES TO CASH MANAGEMENT

Before 2015, the industry’s approach to cash management relied upon short-term funding. As a result, there was not a strong focus on governance and control. Then, between 2015 and 2018, banks diversified their funding sources in response to increased regulatory oversight. The lack of consistent rules across different jurisdictions presents cash managers with compliance challenges.

A Broadridge survey, conducted with Corporate Treasurer Magazine, reveals that the cost of complying with these new regulations is detracting from front-office investment, such as serving corporate treasury clients with tailored and efficient solutions.3 Despite some recent attempts to ease regulations imposed over the past decade, few firms expect a return to the pre-crisis regulatory environment.

“One-third of banks admit they rarely produce accurate forecasts and only 18% are confident their reports are always accurate.”

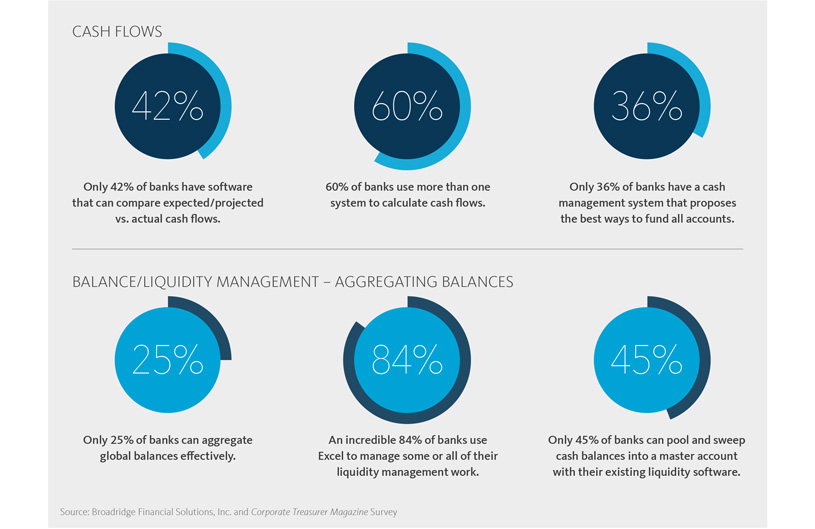

As shown in the following graphics, in addition to meeting regulatory reporting requirements, the Broadridge survey highlighted that treasury departments face internal challenges of balance and liquidity management, cash forecasting, cashflow matching, and payment controls. One-third of banks admit they rarely produce accurate forecasts and only 18% are confident their reports are always accurate. This lack of confidence can be attributed to the fact that over 84% of banks use Excel for some or all of their liquidity management processes. Only 25% of banks can aggregate global balances effectively. Furthermore, over 60% of banks use more than one system to calculate cash flow.

In summary, it’s not unusual, even at a tier 1 bank, for treasury departments to use several systems, some as old as 20 years, stitched together with spreadsheets. Therefore, there is a pressing need for modern technology. IT leaders are seeking an integrated solution as banks adopt a more risk-focused culture with tighter cost controls and greater collaboration across business units. Cash management has evolved from simply keeping track of cash to optimizing working capital and improving balance sheet management. With short term interest rates rising, banks have an additional incentive to invest in new cash management technology because the financial reward for optimizing the value of cash through short term investments is that much greater.

A recent PwC poll reveals that CFOs and treasurers want their teams to be efficient and effective centers of cash forecasting and cash management optimization.4 As shown in the graphic on the next page, these are the top two priorities of treasury departments, ranked above even financial risk management and capital structure. To generate accurate cash flow forecasts, a solution must be able to access balances, positions and trading activity from across the organization. If this information resides in disparate systems or spreadsheets, it is impossible to pull and aggregate this data in real time. Similarly, cash optimization requires real time current and projected balances so fully informed trade and cash transfer decisions can be made. Modern cash management solutions can provide this complete, accurate and timely information.

KEY ATTRIBUTES OF A BEST-IN-CLASS CASH MANAGEMENT SOLUTION

An ideal solution should be able to automate cash-related data and present this information to key stakeholders in a timely and actionable format. Reporting, cash matching, position management, cash forecasting and payment controls are essential requirements. Many existing systems focus primarily on cash forecasting and cash matching but pay little attention to reporting, position management and payment controls. Robust reporting functionality is required for both internal and external purposes. Customizable dashboards must be available for treasurers, cash managers and risk officers so they can monitor balances, track exposures and be alerted to unexpected activity throughout the day. As highlighted earlier, generating accurate regulatory reports is of vital importance due to the potential financial and reputational repercussions of errors. The ability to view and manage positions in real time for the bank and its customers is a key requirement for a modern solution. A global view must include all accounts and positions regardless of where the positions are held, so the user sees a complete view at all times. Payment controls, including “four-eye checks” and exception processing rules, will reduce potential errors while insuring that non-standardized cash movements can still be processed as required.

A fully automated solution, whether it handles 500 or 5 million daily cash transactions, should have user-defined rules and exceptions, integration tools and a user-friendly interface. The goal is to put the power of data in cash managers’ hands, facilitated by an intuitive dashboard. A cash manager should be able to see aggregated account balances globally and drill down into accounts to view customers, currencies and balances as well as individual transactions. Detailed intraday and forecasted balances should also be available. These system capabilities will produce greater efficiency, lower risk exposure, reduced operating costs and increased profitability.

“A fully automated solution, whether it handles 500 or 5,000,000 daily cash transactions, should have user-defined rules and exceptions, integration tools and a user-friendly interface.”

FIVE BUILDING BLOCKS OF AN EFFECTIVE, REAL-TIME CASH MANAGEMENT PLATFORM

As banks seek to replace outdated cash management infrastructures, they are looking for a platform that is flexible and extendible, and delivers these five capabilities: reporting, cash matching, position management, cash forecasting and payment controls

1. REPORTING

Real-time reporting takes care of immediate daily needs, providing accurate intraday data and meeting regulatory reporting demands. Too often, reporting depends on spreadsheets—an approach that may work well for a less regulated organization, but is inadequate for any bank.

2. CASH MATCHING

Real-time cash matching ensures that what a bank believes is being held in its Nostro accounts at other institutions tallies consistently with what those institutions are reporting. Taking intraday feeds from SWIFT, Equant, J.P. Morgan and others5 , parsing them into individual debits and credits, and matching actuals from a transaction processing system gives a true picture of whether cash is matched. This allows resources currently devoted to manual reconciliation to be redeployed to more productive activities, while reducing the chance for costly manual errors.

3. POSITION MANAGEMENT

Proper position management builds upon cash matching; analytics are applied to create a global macro view that advises whether the bank is holding the right balances in the right accounts and how to optimize assets over the longer-term. For example, if an organization is net short across all its euro accounts when funding costs in those accounts are high, the system might suggest using U.S. dollars to buy euros to meet that shortfall and to short dollars because U.S. funding costs are lower. This type of real-time analysis for all cash positions globally helps banks ensure that their cash is in the right location at the right time.

4. CASH FORECASTING

Accurate forecasts of future cash balances can significantly improve the quality of banks’ funding decisions. These projections must be based off real-time cash balances that incorporate the impact of all types of transactions, including movements between money market accounts, wire payments and the settlement of trades. Too often, legacy systems cannot capture all trade types and transfers across every business unit and region so the forecasts are incomplete. Modern solutions can pull data from across the organization and make it available in a centralized repository so cash managers can make fully informed funding decisions.

5. PAYMENT CONTROLS

Finally, banks must optimize which accounts cash is delivered to and which accounts payments are made from. Using a rules-based system, cash can be moved to maximize interest income, minimize fees and mitigate currency risks. For example, knowing the forecasted day-end balance of Nostro account A and Nostro account B will help discern whether it’s smarter to deposit funds into account A or B. At many banks, the decisions to change the normal flow of funds require “four-eye control”— signoff from an operations manager and supervisor. However, an effective solution can go beyond “four-eye control” by identifying exceptions (such as paying funds first into overdrawn accounts) and then writing new rules to handle these exceptions. Such a rules-based and exceptions-based approach minimizes the costs and risks of manual intervention. Most legacy cash management systems cannot address all aspects of payment controls.

FINAL THOUGHTS ON IMPLEMENTING A CASH MANAGEMENT SOLUTION

Onboarding a modern solution can transform the cash management department from a reactive cost center into a proactive profit center. Achieving that goal clearly requires a willingness to invest in technology and reengineer existing processes. However, given the budget constraints at most banks and the rising opportunity cost of inaction while interest rates climb, many organizations find that buying an off-the-shelf solution from a third-party vendor will produce the fastest result at the most effective cost. Since cash management is a non-differentiating function, there is no competitive advantage for a bank to build a bespoke system. Indeed, as recent regulatory changes have proven, it is more beneficial for banks to move to an industry-wide platform that will meet future regulatory needs, mutualizing that cost across many customers.

Corporate Treasurer Magazine supports this “buy rather than build” strategy as it cautions treasury executives not to try to develop best-in-class cash management systems in-house. Instead, they “should consider established solutions in the market that can solve many of [their] issues.” The magazine writes that “financial technology can help make processes more efficient and transparent, and address key challenges while mutualizing costs. This, in turn, will allow cash management professionals to focus on what they are good at—managing cash and payments effectively. This has never been more the case than today. As regulatory compliance absorbs ever more time and intellectual effort, it is increasingly important to know how to ensure that cash management is performing optimally.”6

“Broadridge research reveals that, on average, investments in third-party-vendor cash management solutions that integrate with existing bank systems pay for themselves in 12 to 18 months.”

As banks mull over the right time to invest, the opportunity cost of poor cash management rises with every increase in interest rates. The good news is that there is not a multi-year payback period for these technology investments. Broadridge research reveals that, on average, investments in third-party-vendor cash management solutions that integrate with existing bank systems pay for themselves in 12 to 18 months.