Proxy solutions for funds and alternative investments

Proven proxy performance

-

Manage high-level strategies and individual campaigns

-

Reduce effort with single-source accountability

-

Facilitate effective meetings and leverage data-rich recaps

-

Optimize strategy through fund and shareholder data analysis

-

Use targeted, multi-channel outreach to achieve quorum and passage

-

Project voter engagement using Vote Propensity Analytics

-

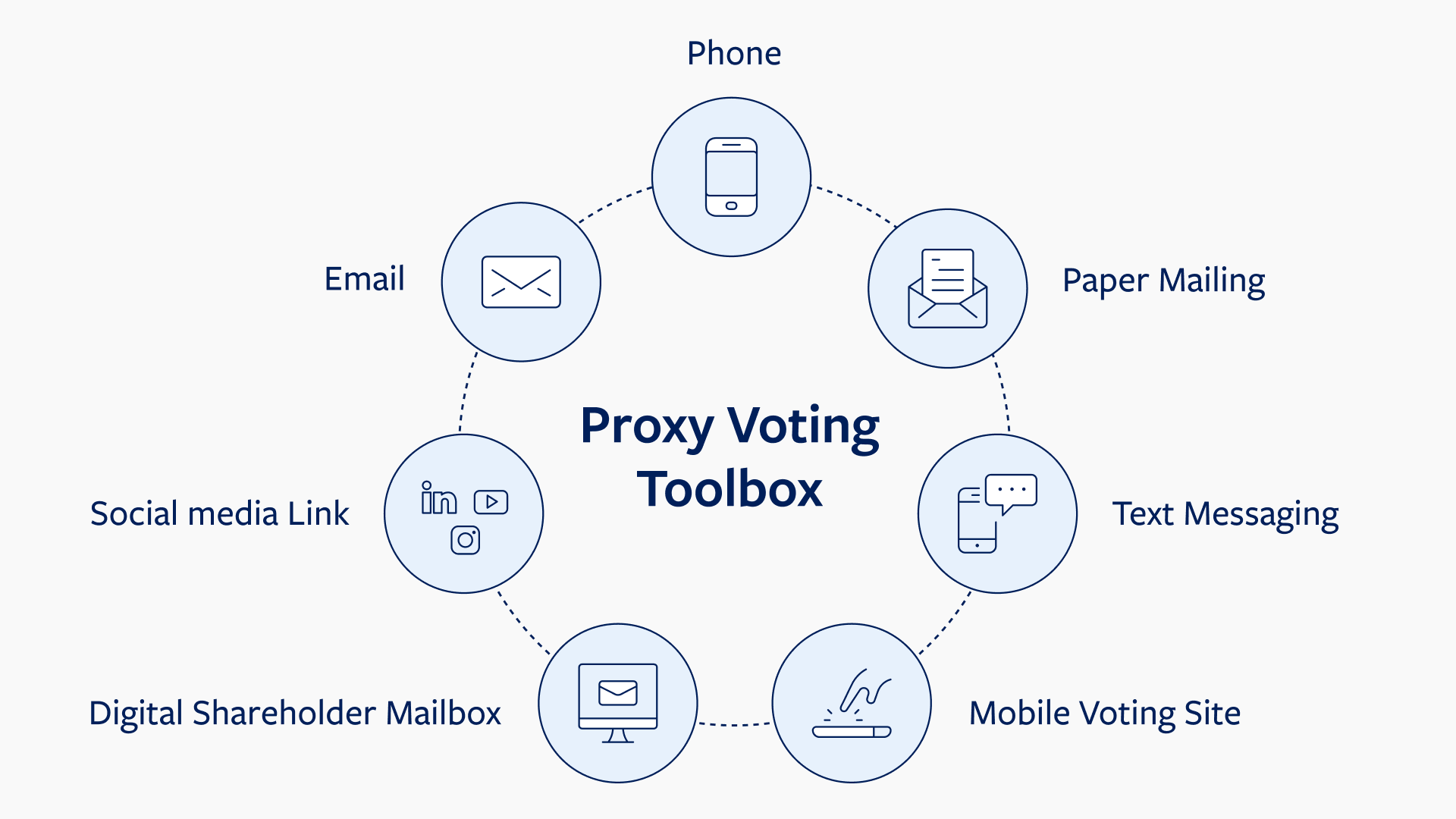

Align communication channels to investor segments

-

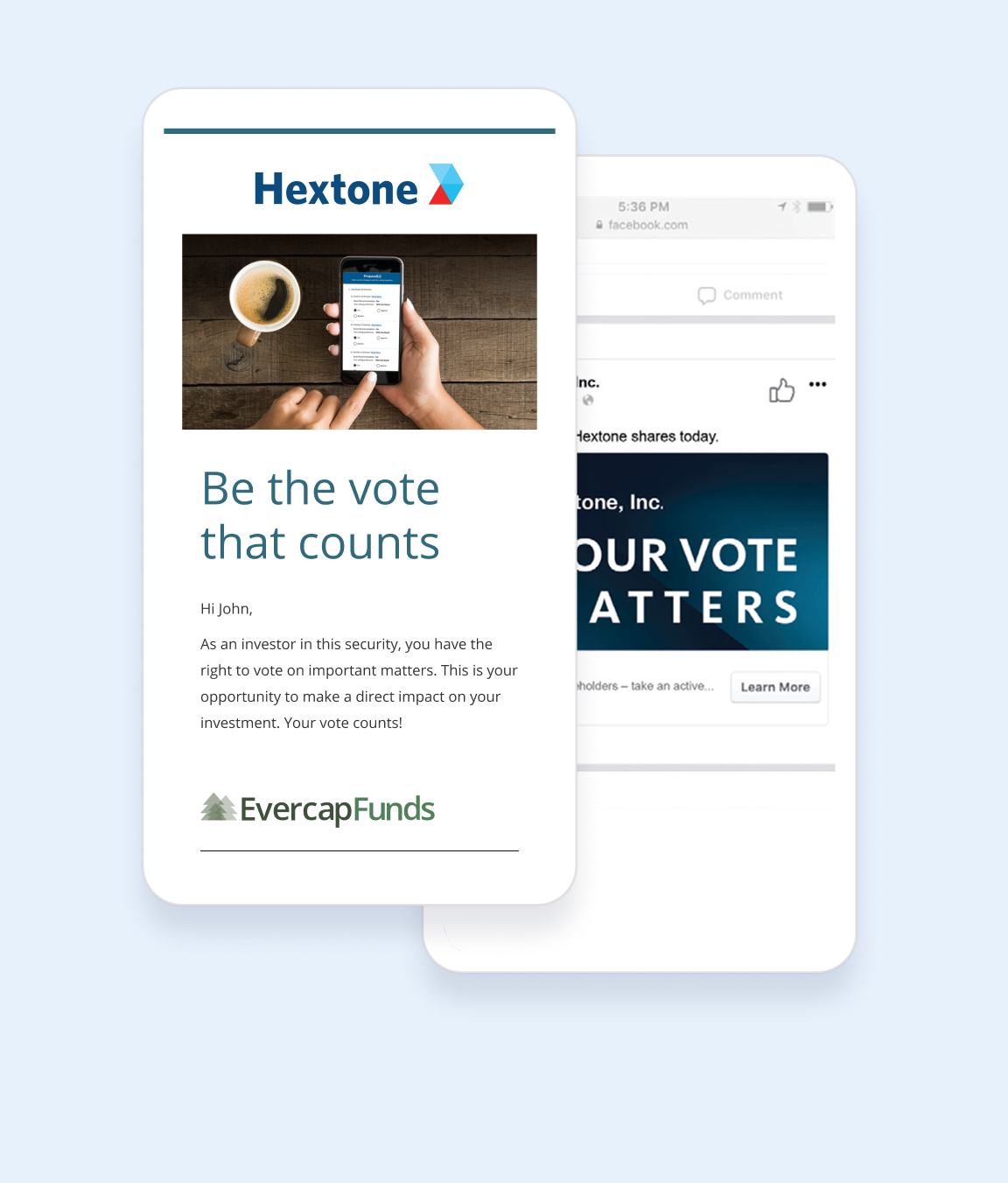

Utilize streamlined emails, social media and text messaging

-

Simplify voting with the ProxyVote mobile app and website

Your comprehensive approach to reaching quorum

Map out your engagement tactics

Assess overall efforts, plan resources, and develop comprehensive strategies and timelines with expert support.

Operate with efficiency

Take campaigns from start to finish with solutions to initiate proxy, process voter data, and execute outreach according to best practices.

Improve campaign status

Tabulate votes and use the data to analyze, assess, and update the strategy as needed. Conduct additional solicitation to capture maximum votes as required.

Maximize meeting attendance

Host virtual shareholder meetings, complete with recaps that include proof of proxy, campaign wrap-ups, and lessons learned for future campaigns.

What's next for your business?

Mutual Fund & Alternative Investment Proxy FAQs

Broadridge provides comprehensive proxy management for mutual funds, ETFs, and alternative investment vehicles, including shareholder communications, vote solicitation, and tabulation.

Yes. Broadridge supports ’40 Act proxy processes, including reorganizations, mergers, and changes in investment advisors, ensuring compliance and efficient shareholder engagement.

Yes. Broadridge’s proxy solutions support voting and tracking across multiple geographies, helping fund managers manage global holdings efficiently.

Broadridge automates the distribution, collection, and reporting of proxy votes, reducing manual effort and ensuring timely, accurate results.

Yes. Broadridge offers detailed product information and brochures outlining its mutual fund and alternative investment proxy capabilities upon request.