Article

Rockall,

a Broadridge Business

read more

Risk and reward do not always have to be polarized. Stress testing is a practical risk management tool that informs senior management, enabling the setting of realistic goals for lending policy and capital allocation while putting a contingency in place for adverse scenarios. The benefits can extend beyond the short-term goal of successfully passing regulatory/compliance reviews and position firms to manage risk and move quickly with the markets.

“Compared to pre-financial crisis spending levels, financial Institutions spend on compliance has increased by over 60% for retail and corporate banks”

Good stress testing isn’t just about “top-down” regulatory compliance at the organizational level. Accurately identifying and scoping risk profiles within the loan portfolio can only help an organization. A thorough “bottom up” evaluation of the portfolio fully prepares the bank for worst-case scenarios while enabling the validation of current lending limits and policies. Ongoing credit stress testing (whether at the level of loan, account, security, group of securities or book) delivers the deep insights needed to drive better business decisions and customer relationship success.

In the case of wealth lending, and SBL in particular, the credit risk environment can change very quickly. Accurate and granular credit stress testing is critical to mitigating and managing credit risk. More than that, wealth managers want to leverage stress testing results to drive efficiencies and opportunity. Intelligent stress testing of the SBL book emerges as a critical business tool – whether to help improve control of concentration risk across the book or flexibly manage credit policy at a loan level to improve the customer experience.

Wealth managers are evolving to respond dynamically to stress testing insights. Detailed sensitivity analysis enables better credit risk management in the loan book. Even within a business line, credit policies can flex as on-boarded collateral affects loan concentration. Understanding those aspects of the portfolio that are vulnerable to sudden market shifts or sectoral swings can influence the direction of credit policy and help managers to make dynamic decisions on portfolio composition – or at least to understand the broader capital and risk impact of loan decisions.

Tough lending decisions are supported by deeper knowledge of the components of the loan book and the relative contribution of one collateral asset class over another. For example, a loan application supported by a portfolio of securities that are not heavily represented in the loan book will diversify the book and potentially offset some concentration risk. Knowing that a borrower’s portfolio of securities will reduce rather than increase concentration risk in the loan book may result in a more favorable credit decision on a loan that, at face value, might have been treated negatively. Likewise, being able to price loans in a way that reflects the impact of the loan on portfolio composition level makes good business sense.

In the case of SBL, when markets move quickly wealth managers need to respond quickly. Severe market volatility or sudden large price moves in a popular stock or segment can trigger a deluge of out-of-margin and top-up events. Knowing what to tackle first and how to de-risk the book quickly is mission-critical.

Wealth managers need to be able to answer the following questions:

Credit stress testing for SBL continues to evolve – encompassing factors like market liquidity, whereby highly-traded securities may be treated more favorably, whether from a loan pricing or advance rate perspective.

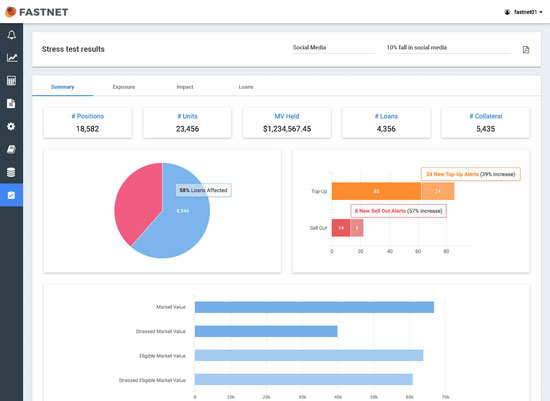

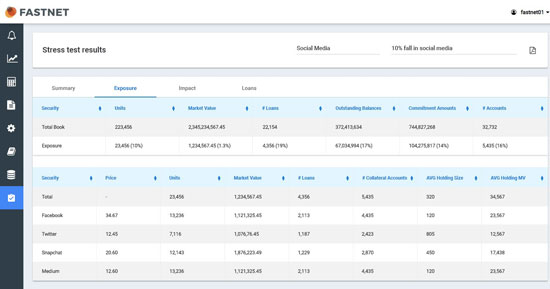

Broadridge offers flexible credit stress testing to help to identify risk indicators, set up contingency plans and refine the capital distribution of securities-based loans. Based on accurate loan data and daily market prices and ratings, Rockall FASTNET, our SaaS solution for SBL, simulates loan book behavior and enables testing for multiple “what-if” scenarios to instantly uncover risk exposures in the SBL book.

Our scenario simulator displays projected impacts on collateral accounts and associated loans, uncovering where the book is particularly exposed to certain securities, or groups of securities including asset classes or geographies. Modeling of out-of-margin volumes and triaging strategies enables future-proofing of your wealth lending strategy.

Preparing for the worst-case scenario strengthens overall performance. Having a detailed handle on credit stress testing and the impact of market reverses and concentration risk in the SBL book improves the strength of the business.

How well-equipped is your organization to undertake granular, business-driven SBL credit stress testing? Broadridge helps banks of all sizes better manage risk and be ready to scale to meet tomorrow’s challenges

Welcome back, {firstName lastName}.

Not {firstName}? Clear the form.