Fortunately, public companies and their shareholders can take steps to avoid escheatment. This brief guide will:

- Describe the basics of escheatment, including the requirements of both the SEC and states

- Outline the steps to take to anticipate and prevent problems

- Explain how you can use transfer agents’ services to avoid unnecessary anxiety and cost

Under state law, escheatment is triggered when securities issuers have had no contact with shareholders over a set period. These laws give the state the right to claim securities and uncashed checks, convert them to cash and keep the cash until such time as the shareholder may reclaim the funds. Many states recognize these reclaimed funds as revenues. Strapped for cash, they have become increasingly aggressive in their escheatment practices. Fortunately, public companies and their shareholders can take steps to avoid escheatment. This brief guide outlines the basics of escheatment and the steps to take to anticipate and prevent problems, utilize transfer agents’ services and avoid unnecessary anxiety and cost.

"Escheatment Defined: Escheat (n.) noun. The reversion of property to the state, or (in feudal law) to a lord, on the owner’s dying without legal heirs. Merriam-Webster Dictionary."

Escheatment Basics

In many states, escheatment is now the third largest line-item revenue source. Delaware, for example, collected $607.1 million from gross unclaimed property receipts during its 2017 fiscal year. According to the most recent state estimates, $248 million of that gross total came from stock taken into custody1.

States like Delaware have become increasingly dedicated to ensuring that companies comply with escheatment laws. Companies face growing responsibilities and liabilities as a result. Compliance activities can also result in some concerning outcomes:

Registered-shareholder complaints

Shareholders become particularly unhappy when they aren’t properly notified before property is escheated and securities or unclaimed checks revert to the state.

Penalties assessed

Aggressive state auditing of securities issuers uncovers enforcement cases that can result in issuer penalties.

General ledger audits

These can be triggered by escheatment audits that uncover non-investment property that should have been remitted, such as uncashed vendor checks or unclaimed payroll funds.

Once items are sent to the state, many states post a notice in the newspaper listing names of those who may be due money. This process is outdated and generally not helpful. While some states try to be more proactive and send letters or email, or offer community events, once property is with the state, it’s liquidated, locking in its value. This can be particularly costly to shareholders who lose the benefit of any further gains.

The Painful Costs of Escheatment

When Merck bought Idenix Pharmaceuticals Inc. in 2014, two French scientists went to sell their shares, expecting a windfall of $13.7 million. Instead, they found that the State of Delaware had declared their stock abandoned five years earlier. Through escheatment, the state had collected their stock, liquidated it and recognized the $1.7 million proceeds as state revenue. The state offered to return the $1.7 million from the sale. The scientists are suing the state, claiming illegal seizure. However, they may never see the $12 million they thought they had earned2.

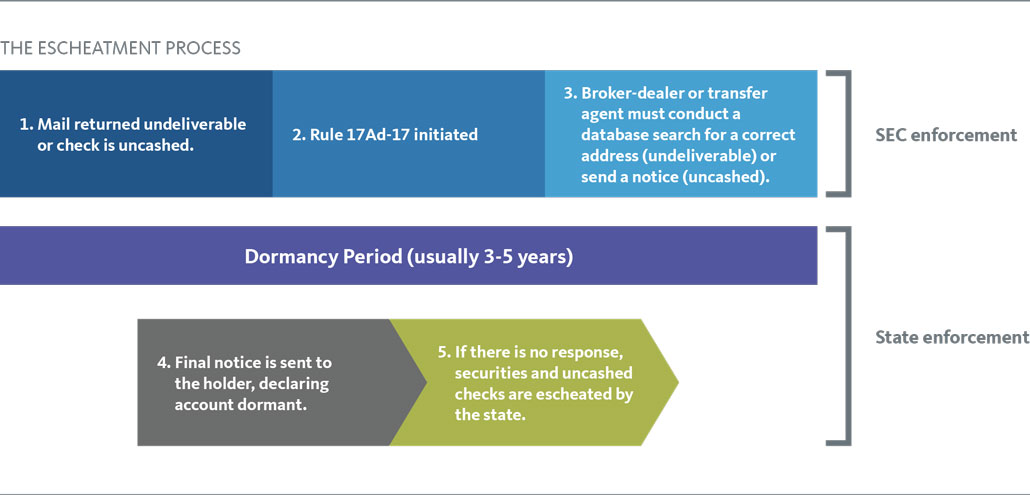

Steps in the Escheatment Process

Now more than ever, companies need to be in compliance to avoid penalties and protect the interests of their shareholders. Fortunately, there are ways to increase escheatment compliance and minimize negative impacts and anxieties. To understand the process, let’s focus first on five terms, each of which can trigger steps leading to escheatment. Registered securities holders may encounter these terms in the sequence shown below.

- Lost security holder – A security holder to whom correspondence has been sent and returned as undeliverable and for whom there is no better address information.

- Unresponsive payee – A security holder who has been mailed a check valued at $25 or more that has remained uncashed for six months or more.

- Dormant account – An account that has passed the state’s applicable period of dormancy. This is a time during which there has been no contact from the owner as evidenced by records of the company or its transfer agent. Prior to remittance to the state, a final notice is sent by the account holder (e.g., brokerage account, transfer agent) to the account owner, declaring the account dormant.

- Abandoned property – Property that has not been claimed by its owner through a request or contact after it has become a dormant account. This property must be reported by the company or its transfer agent to the state of the owner’s last-known address.

- Inactive accounts – An account where the owner has not generated enough activity within a certain period of time. This is probably the area of greatest angst for shareholders. Generations of “buy and hold” investors do not realize that not having any regular contact with a transfer agent can result in their shares or accounts being escheated.

The first two terms above pertain to Rule 17Ad-17 of the SEC. The last two are applicable under state escheatment laws. The period in between the final notice (Step 4 in the process below) and remittance to the state (Step 5 below) is set by state law and varies among the states. In many states, it is 60 days.

Basic Responsibilities

Technically, it is the registered shareholder’s responsibility to provide a deliverable address, cash checks and keep in touch with the transfer agent. However, accounts do go dormant for reasons including change of address, owner’s incapacity or inaccurate data on a transfer agent’s master files. In most cases, shareholders are not aware of the situation until property is escheated. The securities issuer’s responsibility under state law include:

- Tracking unresponsive accounts and strings of uncashed checks through the dormancy period.

- Sending the account owner a final notice prior to reporting the property to the state.

- Turning escheated checks and securities over to the state on a timely basis. (All uncashed checks in a string and the related securities are subject to escheatment.)

For issuers who manage these responsibilities internally, the cost in staff time and money can be significant. There is a value to outsourcing these responsibilities and to educating shareholders.

Stopping the Dormancy Clock

There are several creative ways that transfer agents can proactively attempt to contact shareholders with whom contact has been lost. When successful, these can reset the “dormancy clock” to day zero.

- The transfer agent can insert notifications into proxy statements, encouraging any yes/no vote as an indication of contact. Broadridge has noted a substantial increase in response rates when we have used inserts to generate shareholder activity.

- The shareholder portal can provide proactive notifications to shareholders, urging them with messages such as “update your records” or “vote your proxy”. These messages can pop up each time the shareholder visits the portal until the shareholder initiates contact.

- If companies want their transfer agent to proactively contact shareholders by phone, recorded calls can serve as a record that will withstand a state/Kelmar audit. With proper controls in place, companies can then update the date-of-last-contact in the shareholder’s online record.

Helping to Avoid Escheatment with Proactive Shareholder Contact

If a company is audited by a state or third-party consultant such as Kelmar and Associates, any documented shareholder-initiated contact generally will suffice for avoiding escheatment. In fact, each shareholder-initiated contact “resets the clock to day zero,” for purposes of the dormancy period.

Public companies can educate and remind their shareholders of actions they can take to avoid escheatment, such as:

- Cashing a dividend check

- Having a dividend check electronically deposited through ACH

- Automatically reinvesting a dividend

- Voting a proxy

- Updating shareholder contact information

They can also advise shareholders of the types of shareholder-initiated contact, such as a request to update account records, that generally do not reset the dormancy period.

Shareholder Education

There is value in educating shareholders on escheatment requirements and prevention techniques. For example, an informative FAQ on the Investor Relations tab of your company’s website can provide the insight they need.

Your transfer agent’s relationship managers can also make sure your staff understands the requirements of both SEC and state rules and their associated liabilities. (Note that the two sets of rules have separate, very different requirements that are often confused.)

Shareholder Advice From the National Association of Unclaimed Property Administrators (NAUPA)

As an issuer, it’s a good idea to remind your shareholders of basic tips to avoid escheatment. Here is an example from NAUPA:

“Remember, property becomes lost due to a company having no communication with the owner. You should contact institutions that hold your money or property every year and especially when there is an address change or change in marital status. For security reasons, most financial institutions do not forward mail. Keep accurate financial records and record all insurance policies, bank account numbers with bank names and addresses, types of accounts, stock certificates, and rent and utility deposits.3

Costs and Benefits of Transfer Agent Escheatment Services

You want to minimize the number of your shareholders who ever see an escheatment notice. You can have your transfer agent provide a pre-escheatment analysis, listing all accounts that will become eligible for escheatment in the near future. Your transfer agent can also proactively reach out to update contact records for your VIPs and executives.

Turn to your transfer agent for creative ways to minimize escheatment issues. You should expect proactive shareholder contact and education programs from your transfer agent. Plus, in cases where escheatment is unavoidable, he or she should help you quickly and efficiently meet your responsibilities and minimize liabilities.

It’s best to have an open dialogue with your transfer agent about how escheatment-related services will be billed. Some include them in scheduled costs while others may bill them as extra costs.

We hope this guide has increased your knowledge of the escheatment process, which in turn may help your company meet all requirements of both the SEC and states; and help your shareholders avoid costs and anxieties involved in the loss of personal property.

About the Author

Francis M “Fritz” Rudden, Vice President, Service Delivery, Broadridge. Prior to joining Broadridge Fritz founded Integrated Financial Services Group, Inc (IFSG), a company that specialized in offering annual unclaimed property auditing and reporting services. Broadridge acquired IFSG in 2018. In his current role Fritz provides unclaimed property expertise to public companies and guides them through the annual reporting process.

References

1 https://www.wsj.com/articles/scientists-out-12-million-sue-delaware-over-seizureof-their-stock-1503054001

2 Ibid

3 https://www.unclaimed.org/what/