Trade Matching & Allocation

Achieve real-time, multi-asset trade matching from a single access point. NYFIX Matching facilitates every post-trade allocation, confirmation, and affirmation with unrivaled accuracy.

Accelerate multi-asset matching and post-trade processing

Sophisticated automation

-

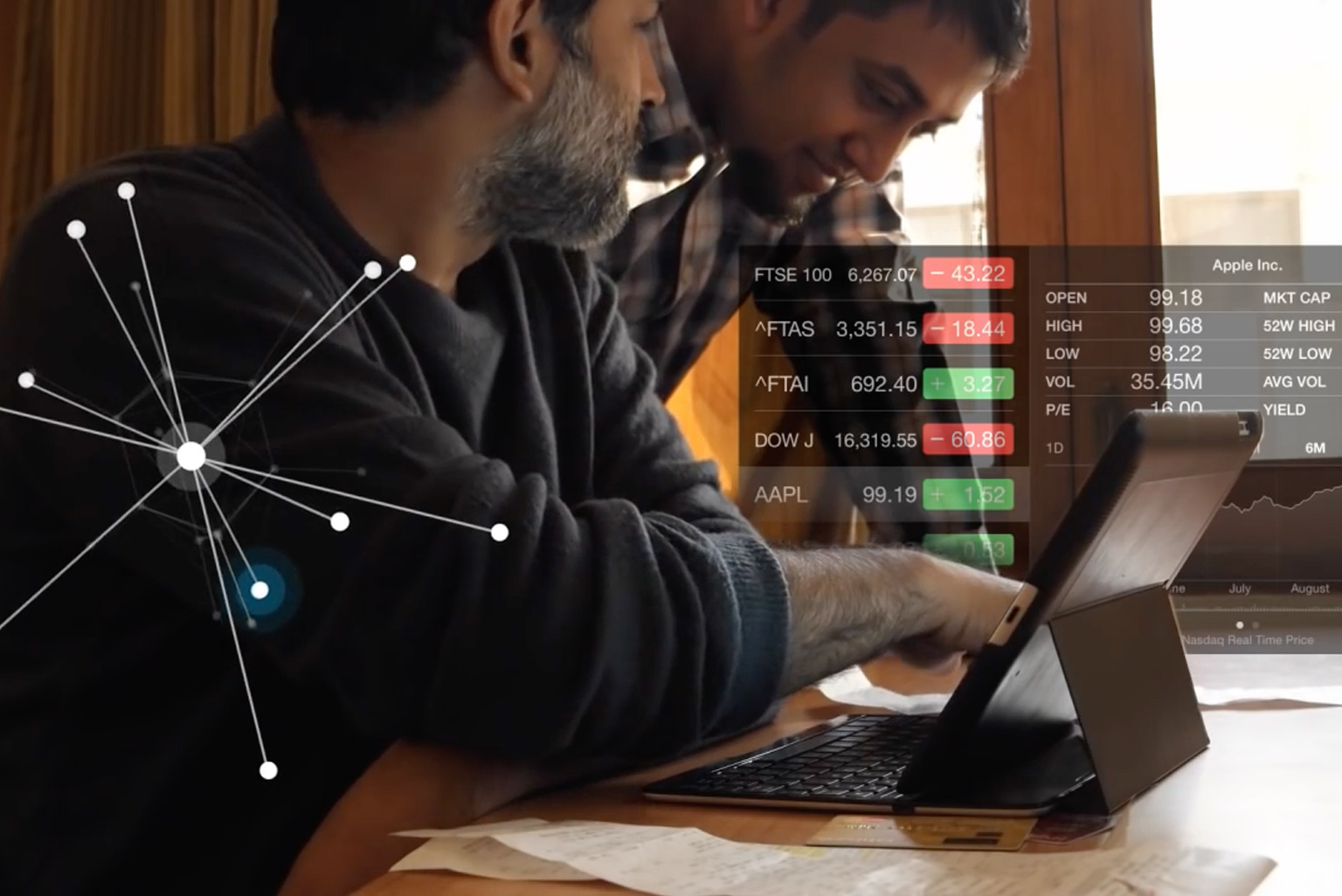

Match trade details between counterparties in real-time

-

Reduce processing times up to 50%

-

Implement rules-based allocation for multi-account and multi-fund trades

Seamless, real-time trade matching

-

View all positions globally

-

Perform block- and allocation-level matching

-

Enable intraday matching using unique identifiers

Scalable, flexible cost efficiency

-

Reduce costs by minimizing end-of-day errors

-

Integrate with your existing OMS

-

Easily scale operations for larger volumes or new regions

Compliance and risk protection

-

Resolve discrepancies with automated exception management

-

Monitor post-trade activities 24/7

-

Achieve 99.9% accuracy in regulatory reporting

Real-time multi-asset trade matching

Related solutions

What's next for your business?

We want to hear more about what you need to improve your business and drive transformative innovation, efficiency, and growth.

Want to speak with a specialist?

North America

+1 800 353 0103(option 3)

EMEA

+44 162 591 9082

Hong Kong

+852 3004 3094

Singapore

+65 31 351 278