Article

Rockall,

a Broadridge Business

read more

Just like color blindness, collateral blindness affects perception – in this case, the way collateral is assessed, aggregated, valued and used. Collateral blindness causes considerable and avoidable loss for banks every year.

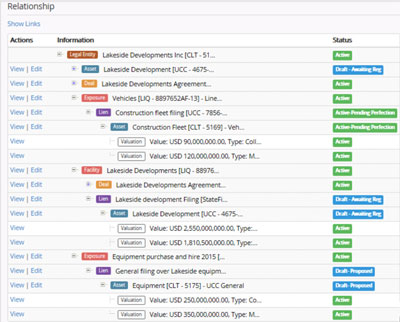

To navigate risk, banks need to know the details of the collateral held against its loans. Most banks lack a data model that exposes collateral data in a way that reveals every nuance and connection. The trouble is, anything less than this inevitably results in an inadequate understanding of the broader loan book – and the true extent of credit risk at play.

Collateral blindness affects most banks, often without them realizing it, in three common ways:

It makes simple business sense to get a firm grip over complex data, relationships and linkages held in the banking book and to manage it dynamically and with reference to the bank’s broader credit landscape.

By implementing an aggregation layer for banking book collateral, accurate and complete information can be put into the right hands. All stakeholders can be satisfied – from operations and business development to product portfolio management, compliance, capital adequacy, treasury and beyond.

Putting a lens on collateral data reveals quality and completeness in granular detail, helping to resolve information gaps and uncover credit risk. A data model that treats collateral in a holistic way and places it at the center of the credit ecosystem is the perfect lens to use for the correct perception of collateral and of the broader credit landscape.

Understanding your collateral challenges and overcoming them not only mitigates loss, but also gets you ready to capitalize on opportunity moving forward.

Welcome back, {firstName lastName}.

Not {firstName}? Clear the form.