BACK TO THE FUTURE

With all of the press and chatter swirling around the concept of model portfolios, it is worth taking a step back to figure out exactly what they are and why they are generating so much attention. In their simplest form, model portfolios are a series of predefined asset allocation pie charts in which a recommended mix of different asset classes are proposed based on a client’s risk tolerance. Over time, these portfolios are rebalanced automatically according to changing market conditions or client circumstances.

These types of models have always been an integral part of the $6.5 trillion investment advisory solutions industry, according to MMI, which is now 25+ years old. In particular, they have figured prominently in packaged mutual fund advisory programs in which an advisor outsources discretionary investment management to an internal investment committee/research team at a distributor. The underlying premise for these programs were to allow the advisor to focus primarily on building client relationships and gathering more assets by outsourcing the portfolio management responsibilities. In effect, the advisor is operationalizing the portfolio construction to spend more time servicing and educating clients. Broker/dealer program sponsors also appreciate mutual fund advisory programs because they minimize the risk of compliance violations and create institutional-level performance for clients. These programs put the responsibility for asset allocation and investment decisions in the hands of staff at the home office.

THE RISE OF MODEL PORTFOLIOS

If we fast forward to today, several drivers are contributing to the recent trend towards model portfolios. Across the industry, advisors, broker/dealers and asset managers each have their own reason for using model portfolios, but they undoubtedly align to provide significant momentum behind this trend.

Before diving into the reasoning behind each of the various industry constituents, it is worth reviewing the choices today’s advisors have when they construct a portfolio:

- Insourcing

– Advisors can build from scratch each client portfolio in their book of business. The implications of this method are lots of time spent building, executing and rebalancing portfolios. This translates into few efficiencies for the advisor.

– Advisors can take a more standardized approach and run their own models via broker/dealer programs such as a rep-as-portfolio or UMA or license their own models to other advisors.

– Advisors, particularly IBDs and RIAs, also have the flexibility to retain discretion and execute models via emerging model marketplaces.

- Outsourcing

– Advisors can use model portfolios recommended by the home office, TAMPs or offered to them by asset managers for the bulk of their business. In this manner, they will be letting go of underlying asset management responsibilities by giving them over to other investment professionals.

For advisors, the business of asset management continues to get increasingly complicated as they balance growing the business while being connected to portfolio outcomes. Rather than scrutinizing every position fluctuation, a growing number of advisors prefer to rely on the models to manage assets and focus their efforts on client building and retention strategies.

Meanwhile, broker/dealers have their own reasons for promoting model portfolio usage. Home offices want more control over the investment process. Model portfolios offer a way to run investment decisions through stringent due diligence processes. For these reasons, the wirehouses would like more FAs to stay faithful to the centralized discretionary decision-making process provided by their growing internal research teams.

Broker/dealers are busy creating new model portfolios that go well beyond the basic asset allocation portfolios that originally were the domain of the packaged MFA industry. Now, a large range of more specialized models (such as ESG, value, growth, alts, and other variations) are available on fee-based platforms as generated by a firm’s internal research group. At the same time, outside models by strategists and mutual fund companies are also being added to distributors’ lineups, this latter activity mostly in the independent broker/dealer channel that affords more choice, by definition, to their advisors.

Finally, asset managers view model portfolios as a new distribution channel of sorts. They provide an avenue for inserting active funds into portfolios to compete against passive funds. Early on, asset managers may have taken a dim view of models since they challenged the utility of the traditional wholesaler/advisor relationship and were unpredictable given inflows and outflows. With the emergence of centralized research groups determining which funds go in to the portfolios, wholesaling organizations have begun shifting the focus from a large number of individual financial advisors (where they have diminishing ability to influence) to a smaller targeted audience of professional buyers at the home office. For some asset managers, this may lead to a total realignment of wholesaler distribution forces. On the flipside, it also may translate into far greater efficiency in terms of fewer, more targeted office visits and more productive relationships with the B/D home-office professional buyer influencing a large number of advisors in the field.

TECHNOLOGY AS A FACILITATOR

In addition to the drivers from the various constituencies as described above, new technologies have enabled asset managers to participate in the model portfolio phenomenon by enabling FAs to take ready-made asset allocation plans and implement them. In effect, this is similar to FAs creating their own personal managed account platform, but at a generally lower cost. In doing so, they are not only competing with traditional Turn-key Asset Management Programs (TAMPs) from a cost perspective, but also they retain discretion over the account. This frees them from the need to outsource investment management to a third-party strategist (TAMP) or home office. Rather, they can implement their own model, or effectively handle their own investment management. For many FAs, maintaining discretionary control over the accounts while simultaneously making the trading and rebalancing more efficient is like having one’s cake and eating it too.

A FRAMEWORK FOR ANALYSIS

To understand which market segments are embracing model activity, it helps to dissect the different types of traditional investment advisory solutions programs. Two types of solutions—rep-as-portfolio manager (RPM) and unified managed account (UMA) programs — are the programs with the bulk of the activity.

RPM programs give advisors the tools to construct investment portfolios using a range of instruments and run them on their company’s fee-based platform. Model portfolio usage is on the rise inside these discretionary programs, which embodies all the trends and key drivers discussed above. In this channel, advisors are realizing opportunities to grow their business and are adopting models available from home offices and asset managers to drive that growth. In many cases, the advisors may utilize the models generated by their firm’s investment research staff, but use these models more as a general framework to build customized accounts for their clients. RPM reps are using some models that are a mix of mutual funds, ETFs and securities for their rebalancing features. At the same time, they may be making manual adjustments to some individual stock holdings to customize the account for the client.

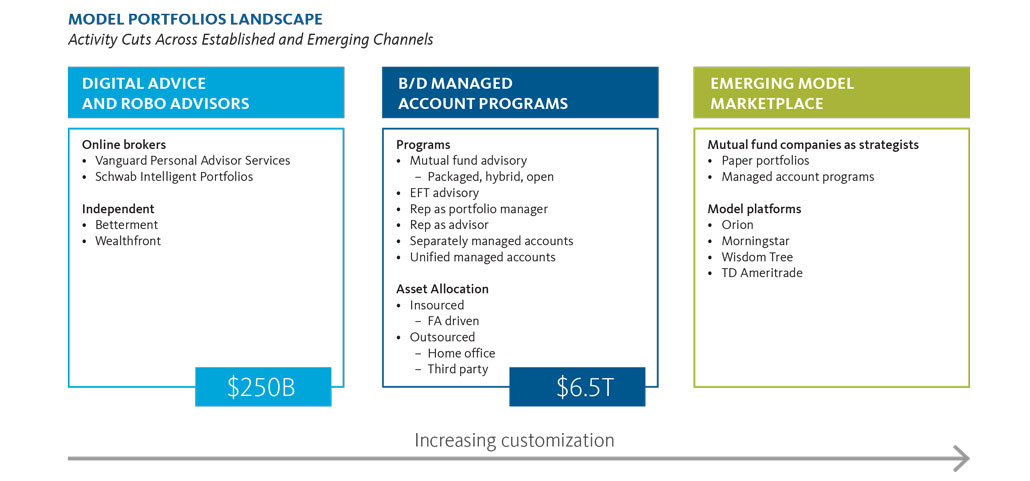

Above is a visual representation of the model portfolio usage landscape. It is organized from left to right in terms of the level of portfolio customization. At far left is the robo-advisor/digital advice marketplace, which we estimate to have roughly $250 billion in assets under management. Here, robo models, akin to the early versions of mutual fund advisory programs, offer a somewhat limited range of models for advice implementation.

Next comes the $6.5 trillion investment solutions industry. Models clearly are part of the discretionary MFA marketplace. Increasingly, we believe that model portfolio activity is happening through a portion of RPM and UMA programs being driven by two major factors. The first is FAs seeking to improve the efficiency of the investment process, while the second is home offices pushing their brand of centralized discretionary decision-making.

On the right side of the visual is the emerging model marketplace, which is a little harder to quantify. Activity within the IBD and RIA channels falls into this segment, as advisors aligned with these underlying channels have the ability to use new technologies not previously available to them to create their own managed account program in which they gain the efficiencies of rebalancing a range of their client accounts at the same time. They are also able to do so at lower cost and retain discretion — something they typically cannot do when using a TAMP.

MARKET SIZING

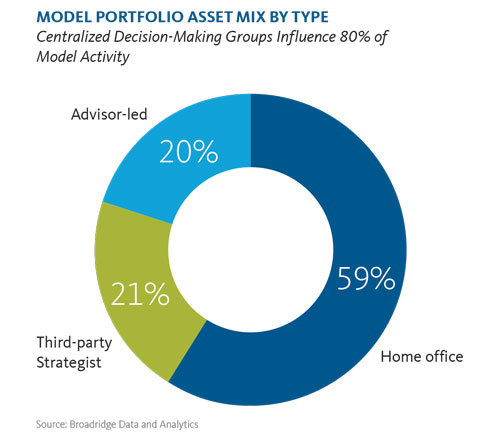

Although asset managers and distributors are actively seeking critically important methods for quantifying the impact of model portfolio usage by advisors, little is known about how exactly to do that at present. In response to this need, Broadridge has developed an artificial intelligence algorithm and applied it to $14 trillion of directly sourced intermediary mutual fund and ETF assets. Our methodology takes a bottom-up view of the entire market and identifies clusters of accounts with the same mix of funds, which collectively we identify as a model. At present, we track nearly $1 trillion in model activity segmented by centralized decision-making group (home office or third-party strategist) or insourced by advisors (advisor-led). Industry-wide, 80% of the model assets we track are controlled by internal research groups and investment committees with the balance allocated and rebalanced by advisors.

CONCLUSION: IMPLICATIONS FOR MANAGERS AND DISTRIBUTORS

Increasing advisor adoption of and reliance on model portfolios certainly has far-reaching implications for the industry. For advisors, model portfolios allow them to build a business that can be scaled, while providing more attention to clients. The open question remains whether advisors will insource the bulk of their investment business as described earlier, or whether they will increasingly outsource and cede control of the assets to a centralized group such as the home office or a third-party strategist.

For distributors, they must continue to invest in their home-office research teams, technology platforms and product capabilities. Some distributors may also choose to develop multiple sub-advised proprietary products to populate their models, as advisors will increasingly rely on in-house research and portfolio models as a way to invest client assets.

Meanwhile, asset managers have an opportunity to focus on creating their own models as a way to deliver their products. At the same time, they may be faced with the possibility that they need to rethink their wholesale distribution organization. Current distribution models that focus on the relationship sales to advisors may be rendered obsolete as the ability to influence the investment decisions are ceded to the home office. Accordingly, proper alignment of sales resources will be needed to drive economics.

As the various players (advisors, home offices and asset managers) converge to drive continued growth in model portfolios each will have to determine what, if any, long term impact it has to their business and adjust accordingly. This is all set against the backdrop of capital markets and changing customer demographics so the outcome remains unclear. What is certain is that success will accrue to those who are monitoring the trends.