The state of play in Asset Management

Firms that are winning these days tend to win big. Those who aren’t — which comprises most asset managers — haven’t expanded their positions or have lost market share.There are three categories that encompass most firms:

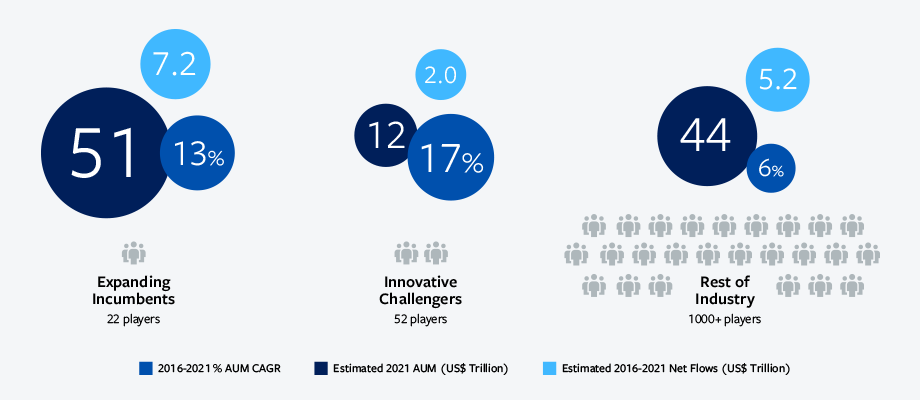

1. Expanding incumbents

Industry players that have maintained, or have grown, their market share. Some 22 managers are responsible for half of the global assets under management (AUM), and half of the industry’s global organic growth.

2. Innovative challengers

Asset managers who have competitive advantages that allow them to grow faster than their peers. Their strategic differences help them offer unique products, distribution, or delivery that sets them apart. These firms only hold 11% of overall industry AUM and less than 15% of five-year net flows, but also have the fastest-growing compound annual growth rate (CAGR).

3. Weaker Competitors

The majority (90%) of asset managers still in weaker competitive positions versus other firms.

Expanding incumbents and innovative challengers account for 64% of the industry’s organic growth over the last five years

What leaders do differently — and what they’ll do next

Not every competitive advantage comes down to investment performance. Solid performance is necessary just to survive in the current market. Firms that want to succeed have to do more: they must adapt to four new competitive dimensions if they are going to make it in an oversupplied industry — faster product innovation, stronger distribution, more flexible delivery, and better brand building.Leaders bring products to market faster

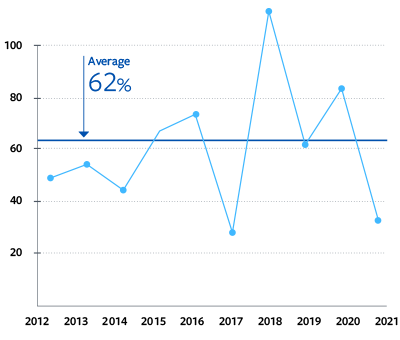

Firms that develop new products quickly are better positioned for long-term growth than those focused solely on large, flagship investments. Although flagship investment capabilities are still the core of the industry’s economics, they’re not able to spur growth on their own. For that, you’ll need to look in less obvious areas of your operations, such as new products.Developing new products can be a challenge. Newly launched funds attracted 62% of net flows every year for the last decade. Only 4% of new products reach the $1 billion mark within five years, however. Of those, only 45% are able to retain or increase the size of the fund after its first year. Firms that can differentiate themselves through products can gain a competitive edge.

Leaders have a better distribution model

The shift toward model portfolios, which hold $5 trillion in the U.S. alone, demonstrates advisors’ appetite for a hands-off approach to portfolio construction. This creates a major opportunity for firms with better distribution; they can offer expertise and advice that advisors are clamoring for. Centralized advice streamlines the delivery process, reduces costs, and improves the quality of advice provided to investors. Firms that do a better job of distribution are poised for success.

Successful competitors realize developing new products is a superpower

Share of worldwide annual net flows from mutual funds launched that year (%)

Advisors are becoming holistic financial planners, not just portfolio managers. Many are realizing managing investor money may not be the best place for them to spend time — they could be out meeting with their clients (and securing new ones).

Leaders are more flexible

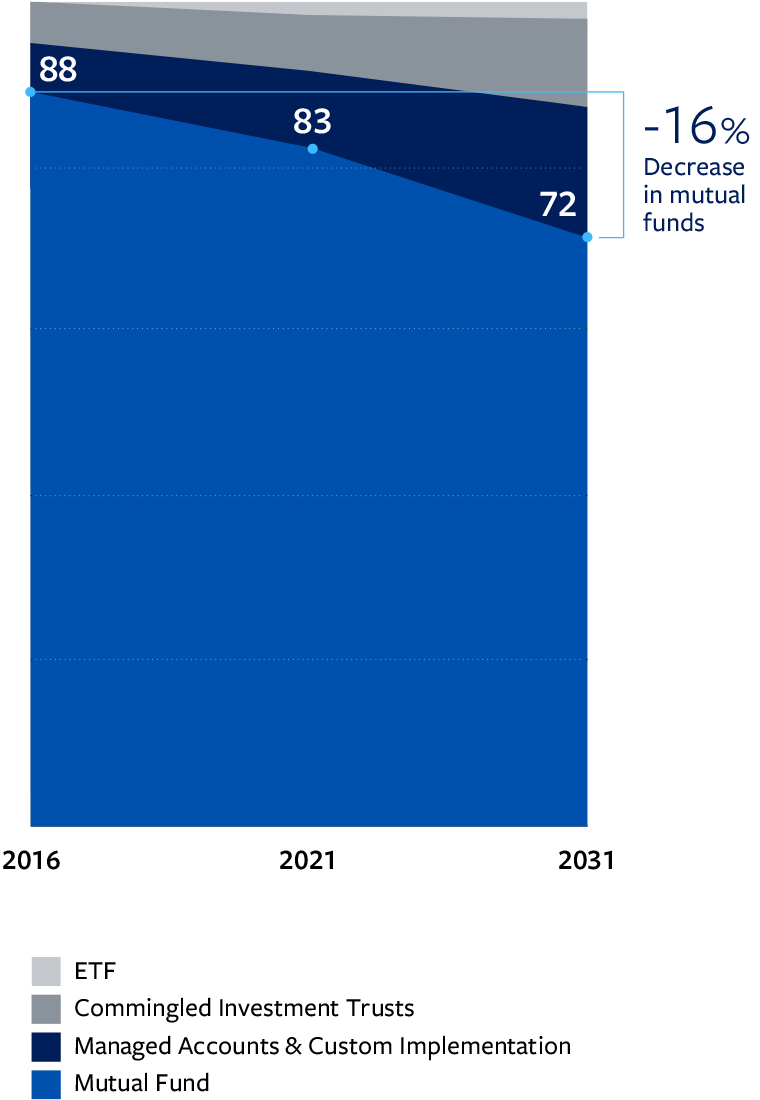

Mutual funds aren’t dead, but they’re far from thriving. New technology has enabled firms to offer an array of alternative investment vehicles that can better satisfy the appetites of today’s investors. The increasing popularity of unified managed accounts, alongside direct indexing and distributed ledger technology, have the potential to eliminate the need for pooled investment vehicles like ETFs altogether.

More individual investors in the U.S. are holding custom-built investment portfolios that are directly managed by asset managers through data-driven portfolio construction and security selection. These technologies and approaches can significantly impact an asset manager's client relationships, the economics of their value chain, and their ability to generate alpha.

“U.S. fund buyers sought the security of tried-and-tested products with regular income components and low risk, while displaying a preference for established brands with a proven track record of high performance,” says Jeff Tjornehoj, Broadridge’s Senior Director of Distribution Insights.

Besides low-risk prime money market funds, which had substantial inflows of $230 billion last year, some of the top categories for inflows were income-producing international income and general bond, and several target-date categories (the “tried-and-tested” portion). Target date funds from 2035 and beyond had inflows of $46 billion not including the retirement channel, such as 401(k)s.

Greater demand for vehicle customization as funds become one of many tools available

Actively managed retail collective fund AUM and custom retail vehicles worldwide excluding alternatives (%)

Leaders have cultivated a distinct brand

If you’re an asset manager, there are only two main ways to differentiate yourself: your investment-related intellectual property and your brand. It’s easy to overlook the latter, but brand building is critical to success.Firms should invest time and budget into building their brand — and that doesn’t mean relying on the usual blend of “trustworthiness,” “client-focused approaches,” and other clichés that don’t help asset managers differentiate. Instead, consider the strategic advantage you offer as your brand-building starting point.

“Asset managers jostled to differentiate themselves by developing their product offering and increasing transparency. But the overall effect was something of a closed shop, as fund selectors doubled down and largely kept their business where it was,” says Tjornehoj.

Those that succeed in this changing market will brand themselves as being ready to handle any of the new products, capabilities, and more complicated use cases we can expect during the next decade. For example, asset managers who fixate on innovation and change should reflect this in the core of their branding. This helps differentiate you versus your competitors.

Don’t just survive — thrive

When you’re able to make the most of these characteristics, you can prime your firm for further growth and capabilities.Technology underpins success in each of these competitive areas. Having a modern technology stack has two benefits. The first is the operational efficiency that up-to-date technology provides. The second is a bit less obvious: new lines of business. Some firms have already established new revenue streams through technologies they initially built for their own purposes.

M&A is increasingly used to help firms broaden their product and distribution efforts, rather than consolidating scale as they might have in the past. Expect standout asset managers to discover firms that complement their own capabilities, since it is relatively easy to acquire and integrate them into an existing framework.

Essential qualities for long-term success

The asset management industry is at a significant inflection point. Four simple approaches will help define success as the industry changes and potentially contracts. Investors are increasingly sophisticated and easy returns are hard to come by in a volatile economy. Firms that focus on these key differentiators will succeed will be faster and more flexible — and they’ll make sure clients know it, too.1 Thrasher, M. (2022, October 13). Asset managers face 'fierce' competition as industry growth slows – report. Pensions & Investments. Retrieved April 5, 2023, from https://www.pionline.com/money-management/asset-managers-face-fierce-competition-industry-growth-slows-report

2 Hickin, P. (2022, August 2). Fuel for thought: Commodity supercycle theory will struggle to pass Ultimate Economic Test. S&P Global Commodity Insights. Retrieved April 5, 2023, from https://www.spglobal.com/commodityinsights/en/market-insights/blogs/oil/080222-fft-warning-signs-energy-prices-metals-agriculture-supercycle